Tungsten – Going Full Force

It is interesting to note that the current division between the Them (China, Russia, Iran and some BRICs) and the collective US. The US used to be the USA and its camp followers, but now in the midst of a shambolic war in the MidEast, the collective US is divided itself into the USA, Israel and the rest. The first to peel off were the Europeans, tired by the barrage of sticks (and a few carrots) that rained down on them before the first schoolgirl had been bombed. It is looking like the dreaded breakup of NATO might come as a blessed (and cathartic) relief to all concerned.

In these bellicose times, if we had to choose a metal to crown as the military metal par excellence it would undoubtedly be Tungsten for its usage in shells/missiles and in armour-plating to resist said shells.

On the eve of the current Tungsten renaissance, there were a (small) tattered army of survivors that had spent a decade in the wilderness. There were only two producers listed in Western stock markets. The Chinese dual-use export ban brought a small number of new players into the space. Interestingly, most of these are focused on past producers, with promoters for once realizing that greenfield exploration was “for the birds”.

It’s worth noting that, of all the critical metals in the military sphere, it is Tungsten where the Europeans find themselves best positioned and, inarguably, way ahead of the US. Tungsten’s main source since its rise to industrial usage has been the Iberian Peninsula. This produces an interesting history which has relevance today because, following the invasion of the Soviet Union, Germany became dependent on Portugal and Spain for their Tungsten supplies, due to its value in producing war munitions. But then again so did Britain. This prompted a massive tug of war over Portugal, and to a lesser extent Spain, over who they would supply to while maintaining a pseudo-neutral status. In this story lies a good example of our “supply & deny” watchwords.

The irony is that Europe finds itself way ahead of the US in Tungsten production with operating mines in Portugal, Spain and Austria. The UK is soon to be added to this group of producing nations. None of this is by design, we might note, but rather historical momentum. The potential to turn back on substantially more production in the Iberian Peninsula (and the UK) is particularly poignant.

Tungsten production was almost driven out of Europe but the stalwart efforts of Almonty Industries Inc. (NASDAQ: ALM | TSX: AII | ASX: AII | FSE: ALI1), backed by powerful players in the machine tools industry that kept operations on the road by paying over the depressed market prices to keep themselves free of the Chinese threat to their fundamental businesses.

Almonty’s main operation is the Panasqueira mine in Portugal which moved into poll position amongst European Tungsten mines when Almonty’s other operation, Los Santos (which we visited and wrote up in 2015), which is in north-west Spain, came to the end of its mine-life recently but is now being rebooted as a tailings reprocessing operation. The company is keeping its powder dry thus far on the greenfield Valtreixal mine/project, which is relatively near to Los Santos.

Wolfram Bergbau operates the Mittersill mine in Austria (near Salzburg) that has been functioning since 1976. A company called Allied Critical Metals Inc. (CSE: ACM | OTCQB: ACMIF) is trying to revive two old Tungsten mines in northern Portugal. These being the Borralha and Vila Verde Tungsten Projects.

Other Tungsten assets have been through the meatgrinder of financial travails and bankruptcy. Wolf Minerals went bankrupt on its Hemerdon Tungsten/Tin mine in south-west England. Hemerdon then passed into the hands of Tungsten West plc (LSE: TUN). Ormonde Mining came to grief on the Barruecopardo mine in Spain and that asset passed, through private equity hands (Saloro), to EQ Resources Limited (ASX: EQR) that had revived Mt Carbine in Queensland. Meanwhile, W Resources plc, holders of the La Parrilla mine in Spain (which now features in the EU wishlist), delisted from the London Stock Exchange, disappearing from (investors’) sight.

Tungsten is, poignantly, the element that has achieved the most with the least support from the Brussels nomenklatura.

Tungsten in North America

The US has quite a strong potential to advance in Tungsten even if it cannot catch up with Europe any time soon. Canada has two contenders in the developer space (Fireweed Metals Corp. (TSXV: FWZ | OTCQX: FWEDF) and Northcliff Resources Ltd. (TSX: NCF)) but both are gargantuan or challenged in other ways (e.g. location and jurisdiction) not to mention eye-watering capex numbers. There is also an explorer worth noting, Fox Tungsten Ltd. (TSXV: FOXT), in British Columbia.

All the US players that we give credence to, American Tungsten Corp. (CSE: TUNG | OTCQB: TUNGF, Guardian Metal Resources PLC (LSE: GMET | OTCQX: GMTLF) and the aforementioned Almonty, have past-producing mines in the Western US. American Tungsten, in Idaho, is a relatively new entrant into the fray. Its shareholders didn’t have to transit the valley of death that the more long-lived participants experienced. However, because it managed to get its hands on a past-producing asset with a relatively short time to reactivation, it has advanced itself up the rankings faster than many other players.

The picture is relatively similar with Guardian, which has two past producing assets in Nevada, with the Tempiute project appearing to be quite plug-n-play. The London-listed GMET also just secured a NASDAQ listing, following in Almonty’s footsteps. The latter, which redomiciled to the US last year, also just added a Montana past-producing asset to its armoury (pardon the pun).

There is a fourth company with an ASX-listing but we cannot be bothered highlighting its scant virtues as it was so low down the pecking order that we had not been able to distinguish it from pond scum. We spoke to several companies in the sector when we had heard outlandish (negative) claims about them and this was attributed by aggrieved managements to this rogue set of corporate slanderers. We later heard they had tried to leave their past misdeeds behind them by changing their name from something totally inappropriate to something overweening and pompous. They shall go on being ignored by us.

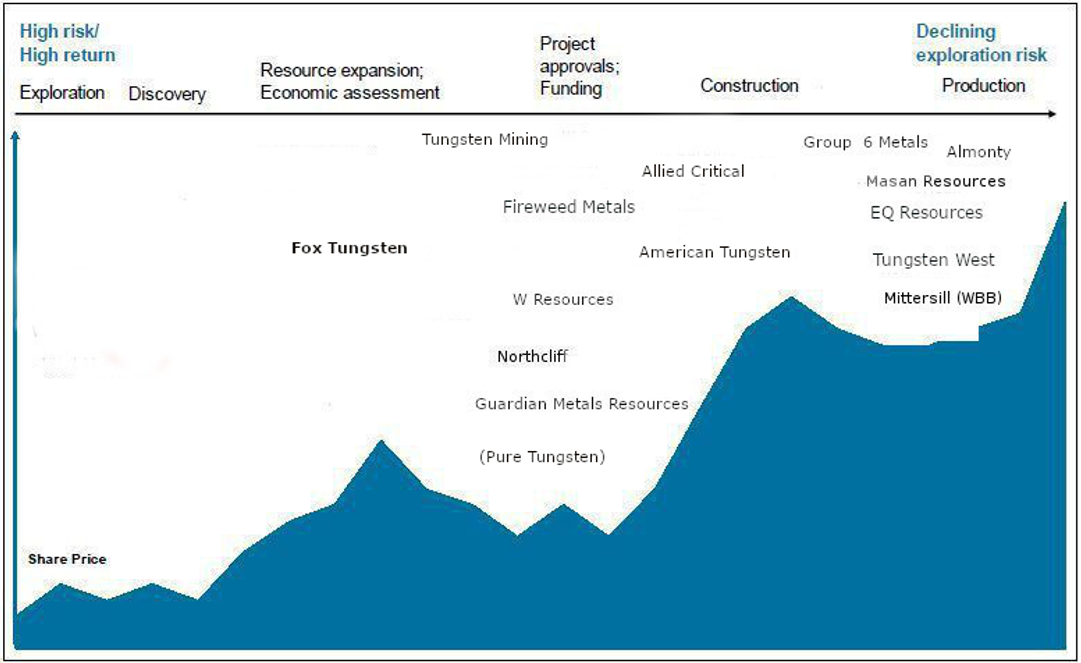

The Tungsten Lifecycle Chart

Our Lifecycle chart, shown below, serves particularly well, in the case of Tungsten, to show the state of progress of the various players vis-à-vis each other on the exploration-production continuum.

In many of the latest go-go metals there are many players that are not serious about getting to production, whereas in Tungsten the culling of the ranks has left only the most determined players. Moreover, it is very rare in charts such as that above that there are so many at the production end of the continuum that we run out of space.

Summing Up

As we have noted the Tungsten space is weighted towards mainly serious (producing) companies that have walked across broken glass over the last 10-12 years to remain in the business and reinforce their commitment to a metal that they believed was pivotal to Western economies and Western militaries, even when those two consumer groups did not know themselves how vulnerable they were to Chinese Tungsten squeeze tactics.

While much verbiage is dedicated to the US’s mighty military-industrial complex, we might almost say that the closest that Europe comes to achieving self-reliance in any critical metal is in Tungsten. The EU’s much touted Circular Economy concept is defective here, though, as little Tungsten is recyclable, particularly that in munitions.

In this hare & tortoise race, the EU tortoise has pulled well ahead and its up to the US hare (to mix a metaphor) to pull its socks up.