China’s Mine‑to‑Magnet Architecture and Global Strategic Leverage

Over the last 40 years (!) China has built five overlapping, vertically integrated rare earth magnet ecosystems, each spanning mining, separation, metalmaking, alloying, and NdFeB magnet production. This is not a single supply chain but a redundant national architecture engineered for resilience, scale, and geopolitical leverage. No other nation possesses even one complete mine‑to‑magnet chain at an industrial scale.

China’s Five Ecosystems are:

- China Northern Rare Earth (Group) High-Tech Co., Ltd. (SSE: 600111): Global NdPr anchor; Bayan Obo is the world’s largest light rare earth element (REE) producer, even though the REEs are largely a byproduct of primary magnetite (iron ore) production.

- China Rare Earth Resources and Technology Co., Ltd. (SZSE: 000831) / China Minmetals Corporation: Controls nearly all domestic Chinese heavy REE (Dy/Tb) ionic adsorption clay deposits; effectively the only scalable coercivity-element supply chain on Earth. (Note: China today imports most of its heavy rare earths — and a significant amount of light rare earths — as concentrates produced in Myanmar, with which it shares a border. The separation and purification of these imports are almost entirely performed in China, primarily at facilities owned or controlled by China Rare Earth Group / Minmetals.)

- Shenghe Resources Holding Co., Ltd. (SSE: 600392): Global feedstock aggregator; integrates purchased production from overseas mines (including, historically, feedstock associated with MP Materials Corp. and Serra Verde Group) into China’s midstream rare earth processing ecosystem.

- Beijing Zhong Ke San Huan High-Tech Co., Ltd. (SZSE: 000970): One of the world’s largest producers of high-end sintered NdFeB permanent magnets; functionally integrated through state-allocated feedstock systems.

- JL MAG Rare-Earth Co., Ltd. (SZSE: 300748 | HKEX: 06680): One of the fastest-growing EV and wind-energy magnet manufacturers/exporters globally, with deep alloying expertise and OEM-grade production capabilities.

Choke‑Point Control (2020s)

- Mining: ~60% global REE ore

- Separation: ~90% of global capacity

- Metal: ~95% of Nd/Pr metal; ~100% of Dy/Tb metal

- Alloy: China dominant; only country with full EV/wind‑grade alloying

- Magnets: 85–90% of global NdFeB output

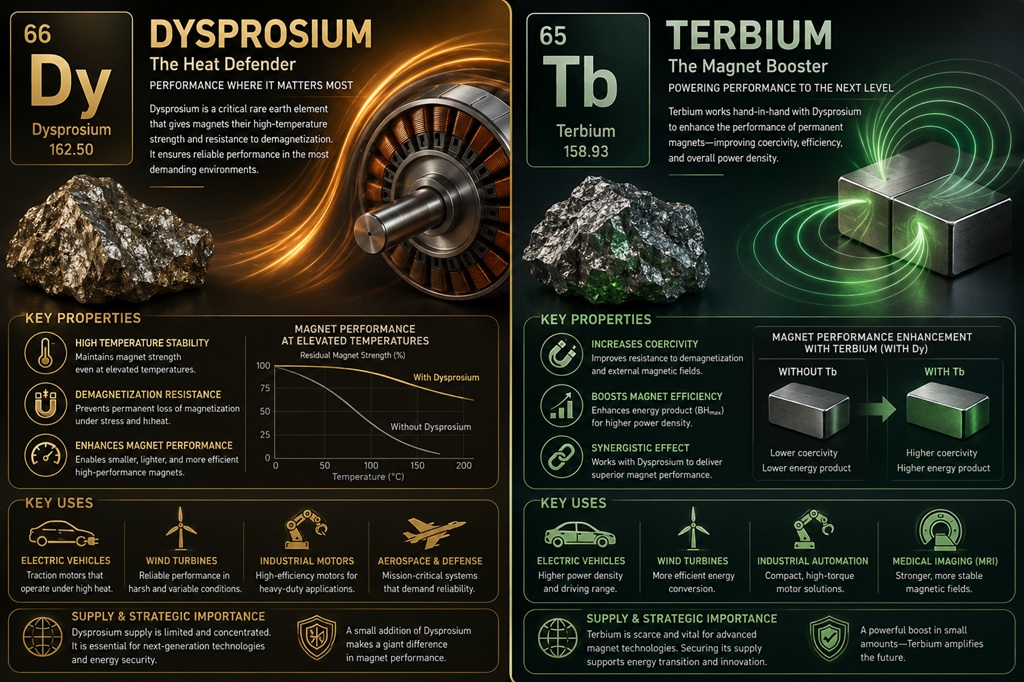

China’s dominance is deepest in Dy/Tb, the coercivity enhancing elements essential for EV traction motors and direct‑drive wind turbines, although today almost all of China’s supply of Dy/Tb comes from Myanmar.

1990s vs 2020s Shift

- In the 1990s: Japan controlled separation, metal, and the manufacturing of high-end magnets; the U.S. produced significant amounts of rare earth ore; China was a low‑cost oxide supplier due to its low cost separation facilities.

- By the 2020s: China controls every stage from ore to finished magnets, with multiple redundant chains and global offtake control.

Implications for the U.S., Allies, and Industry

- Defense: Precision‑guided munitions, radar, actuators, and propulsion systems depend on Chinese produced Dy/Tb.

- EVs: No non‑Chinese supply chain can meet projected U.S./EU EV magnet demand.

- Wind: Direct‑drive turbines require high‑coercivity magnets; China is the sole scalable source.

- Industry: Robotics, automation, and medical devices face structural exposure.

Strategic Reality

Mining is not the bottleneck. The bottlenecks are:

- Separation

- Metal production

- Alloying

- High‑performance magnet manufacturing

- Dy/Tb availability

Required Actions (for governments, OEMs, and investors)

- Build domestic separation + metal plants before new mines.

- Co‑invest in alloy + magnet capacity with OEM backing.

- Develop Dy/Tb substitution pathways (GBD, Ce‑rich magnets, ferrite hybrids).

- Establish rationally organized strategic stockpiles for Dy/Tb and NdPr metal.

- Mandate domestic magnet content for defense and critical infrastructure.

Bottom Line

China’s rare earth magnet dominance is not an accident — it is a 40‑year industrial strategy that created the only complete, scalable, and redundant mine‑to‑magnet architecture on Earth. The West’s vulnerability is structural, not cyclical, and cannot be solved by mining alone.