Critical Minerals Report (05.24.2026): National Security Moves Downstream

The critical minerals sector spent the past week confronting a reality that many policymakers continue to resist publicly: the global race is no longer centered on discovering deposits. It is now about controlling processing, magnet manufacturing, inventory systems, financing structures, and ultimately the industrial architecture that sits between geology and national power.

Rare earths and permanent magnets dominated the week’s developments, but not because of new discoveries. Instead, nearly every major headline — from Canberra to Washington to Beijing — pointed toward a rapidly accelerating struggle over supply chain control, industrial sovereignty, and strategic leverage. The underlying issue remains unchanged: despite years of rhetoric about diversification, China still overwhelmingly dominates the global rare earth ecosystem, particularly the magnet midstream that modern defense systems, electric motors, robotics, AI infrastructure, and advanced manufacturing increasingly depend upon.

The week opened with growing discussion around the structure of the permanent magnet supply chain itself, including renewed attention to the extraordinary concentration of rare earth processing and magnet manufacturing capacity inside China. Recent analysis circulated throughout the sector — reinforced by International Energy Agency (IEA) data showing China’s overwhelming dominance in rare earth refining and permanent magnet production — framed many of the developments that followed over the course of the week (Financial Times — Deal rush in rare earths as West seeks to loosen China’s grip). That concentration became increasingly difficult to ignore as governments, investors, and industrial groups across multiple jurisdictions accelerated efforts to secure alternative supply chains outside China’s orbit.

The Financial Times reported a growing “deal rush” in rare earths as Western governments, industrial groups, and investors attempt to loosen China’s grip on critical supply chains. Yet beneath the optimism surrounding these transactions sits a more sobering reality: the West is not simply attempting to build mines. It is attempting to recreate an industrial ecosystem that China spent decades constructing through coordinated industrial policy, subsidized capital, technical workforce development, environmental trade-offs, and vertically integrated manufacturing. That distinction matters enormously.

The market increasingly appears to distinguish between simple mineral exposure and vertically integrated “mine-to-magnet” platforms capable of participating across the full rare earth value chain. Recent attention surrounding USA Rare Earth, Inc. (NASDAQ: USAR) reflects that broader shift. In January, the company disclosed that it had signed a non-binding Letter of Intent with the U.S. government outlining a proposed financing package totaling approximately US$1.6 billion, including roughly US$277 million in proposed federal funding support alongside a proposed US$1.3 billion loan facility tied to domestic rare earth development. According to the company’s SEC-filed materials, the proposed funding structure is intended to support an integrated U.S. supply chain spanning the Round Top heavy rare earth deposit in Texas, rare earth separation and processing infrastructure, approximately 10,000 tonnes per annum of rare earth metal, alloy, and strip-casting capacity, and 10,000 tonnes per annum of NdFeB permanent magnet production capacity.

The broader significance extends beyond any single company or analyst upgrade. Increasingly, Washington appears willing to use state-backed financing structures, strategic lending mechanisms, industrial subsidies, and procurement policy to accelerate domestic critical mineral and magnet supply chains that would likely struggle to compete economically against established Chinese infrastructure under conventional market conditions alone.

That policy acceleration is occurring even as operational realities remain deeply unresolved.

One of the week’s most consequential developments involved mounting pressure from U.S. defense contractors seeking delays to Washington’s impending restrictions on Chinese rare earth magnets. The Financial Times reported that defense groups are increasingly concerned about the feasibility of complying with Department of Defense sourcing restrictions scheduled to tighten in 2027. The concern is rooted in the scope of the underlying regulation itself. Under U.S. DFARS Rule 252.225-7052, Department of Defense contractors will, beginning January 1, 2027, be prohibited from supplying systems containing certain rare earth permanent magnets—including neodymium-iron-boron (NdFeB) and samarium-cobalt magnets—if the materials were mined, refined, separated, melted, or manufactured in China. The regulation reaches deep into the supply chain and effectively attempts to exclude Chinese participation across the full magnet production process. The issue exposes a widening disconnect between political timelines and industrial readiness, as Western governments continue to accelerate strategic decoupling efforts despite limited ex-China processing and magnet manufacturing capacity currently available.

Jack Lifton, Co-Chair of the Critical Minerals Institute (CMI), framed the issue bluntly during our discussions this week, arguing that many policymakers continue to misunderstand the rare earth supply chain itself. “The complete lack of understanding of the rare earth permanent magnet supply chain by Washington’s capital wasters,” he remarked, “is only exceeded by their lack of understanding of mineral economics, facility design and construction time.” The observation may sound harsh, but it captures a growing concern within the sector that political narratives are advancing faster than physical industrial capacity.

That tension became even more visible as Reuters reported that China would maintain its export-control regime on rare earths and related technologies despite limited diplomatic progress with the United States. Beijing characterized its restrictions as lawful national security measures and indicated it would only consider “reasonable” civilian requests. In practical terms, the White House appears to have secured procedural flexibility rather than structural change.

The distinction is critical.

Over the past several years, Western policymakers often framed Chinese export controls as temporary trade measures or geopolitical bargaining tools. Increasingly, however, Beijing appears to be institutionalizing strategic minerals policy as a permanent component of national industrial security strategy. Bloomberg reported this week that China is moving to tighten oversight of strategic mineral supply and security, reinforcing the broader trajectory toward centralized state control over critical resource flows.

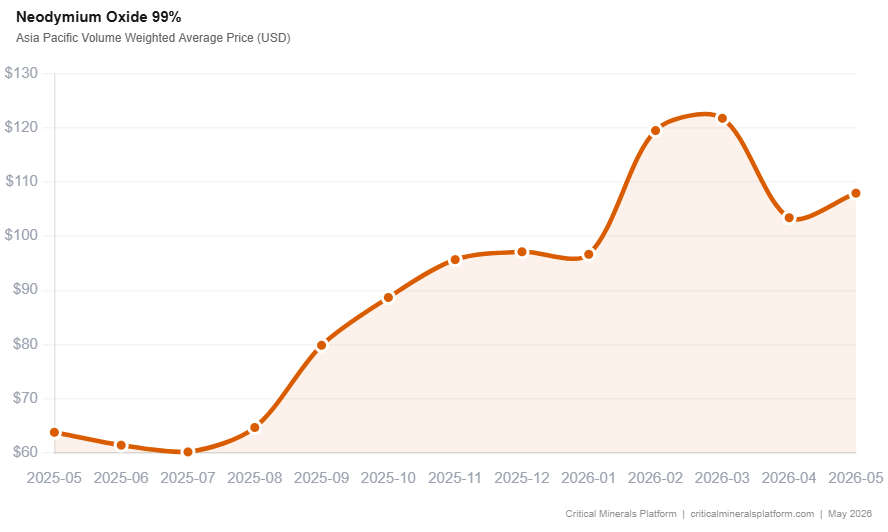

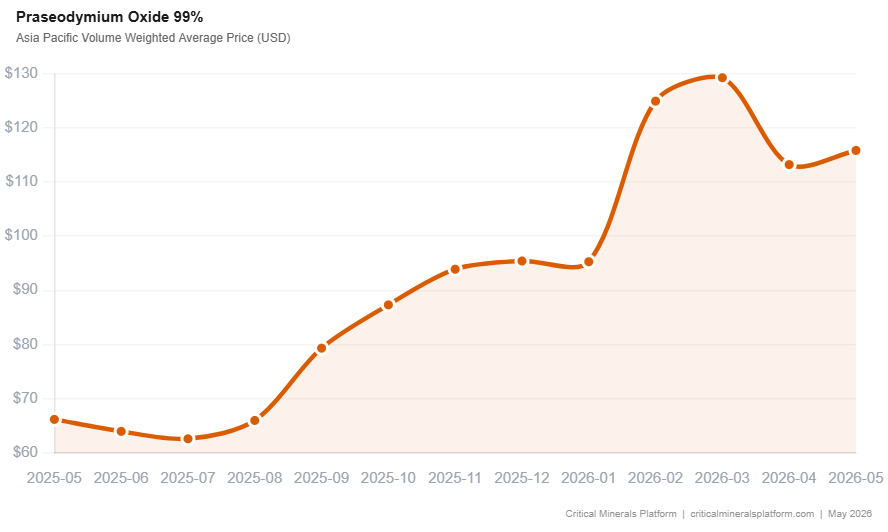

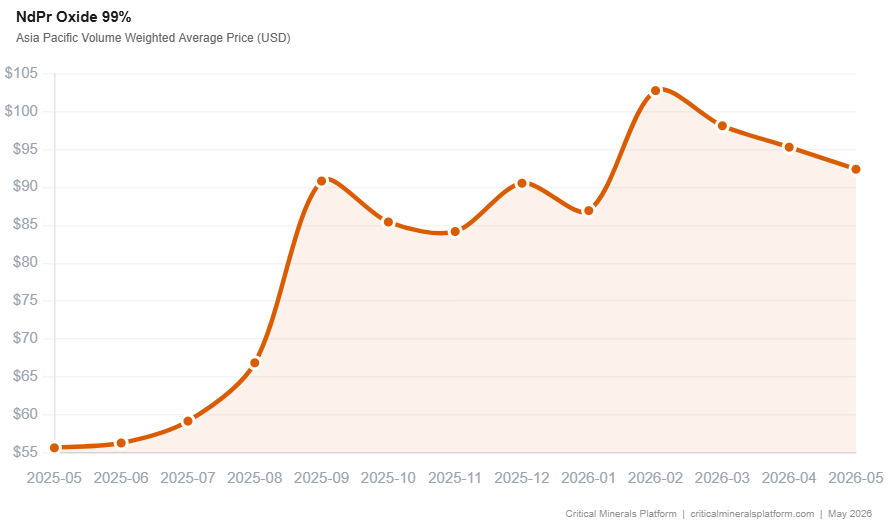

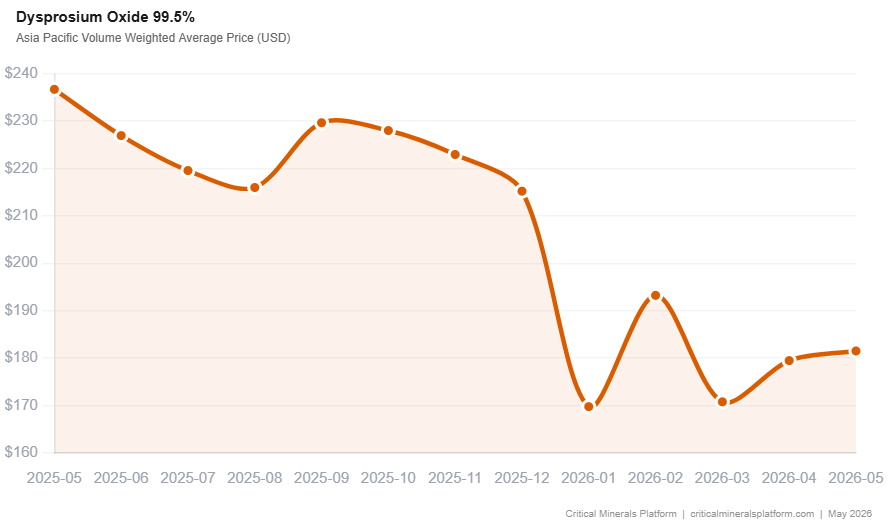

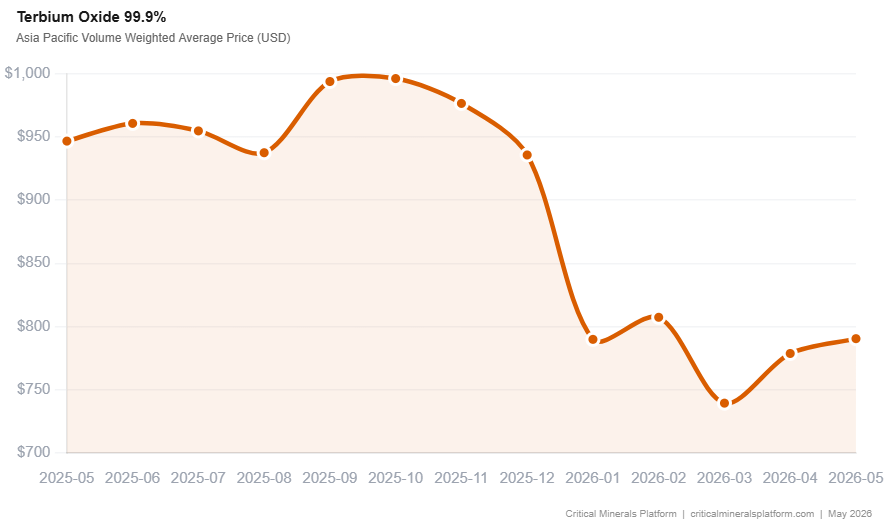

Simultaneously, reports emerged that China had effectively restricted several heavy rare earth exports to Japan for months amid growing regional tensions. The development served as a stark reminder that heavy rare earth supply outside China remains extraordinarily limited. The global conversation often focuses on neodymium and praseodymium (“NdPr”), but the true bottleneck increasingly appears to reside in dysprosium, terbium, and the associated separation and metallization infrastructure required for high-performance permanent magnets.

This distinction also helps explain why Australia emerged as one of the week’s most important jurisdictions.

Canberra took the unusually aggressive step of ordering Chinese-linked investors to divest holdings in Northern Minerals Limited (ASX: NTU), developer of the Browns Range heavy rare earth project in Western Australia. The intervention represents one of the clearest examples yet of Western governments treating critical mineral ownership structures as matters of national security rather than conventional commercial investment.

Australia simultaneously continued advancing offensive industrial strategy. Reuters reported that Arafura Rare Earths Limited (ASX: ARU) formally approved development of its A$1.6 billion Nolans rare earths project in the Northern Territory. The project is expected to produce approximately 4,440 tonnes annually of NdPr oxide and has secured support from export credit agencies across multiple allied jurisdictions, including the United States, Canada, Germany, and South Korea (Source).

The financing structure surrounding Nolans may prove as important as the project itself. The rapid progression from final investment decision to equity financing demonstrated that strategic mineral projects with aligned geopolitical positioning can increasingly access capital pools unavailable to conventional mining developments. Gina Rinehart’s Hancock Prospecting Pty Ltd further expanded its involvement in the sector while simultaneously increasing exposure to U.S. defense-related investments, reinforcing the increasingly blurred lines between mining, industrial policy, and defense supply chains.

Jack Lifton noted this week that Australia’s policy approach appears notably more coordinated than that of the United States. The release of the 2026 Progress Report from Australia’s Critical Minerals R&D Hub reinforced that perception. The initiative integrates multiple national scientific and technical agencies under a coordinated framework focused on processing technologies, supply chain optimization, and industrial competitiveness. “The U.S. has multiple agencies doing this piecemeal with no coordination,” Lifton observed. “Australia, because its economy is so dependent on the export of critical raw materials, is more focused.”

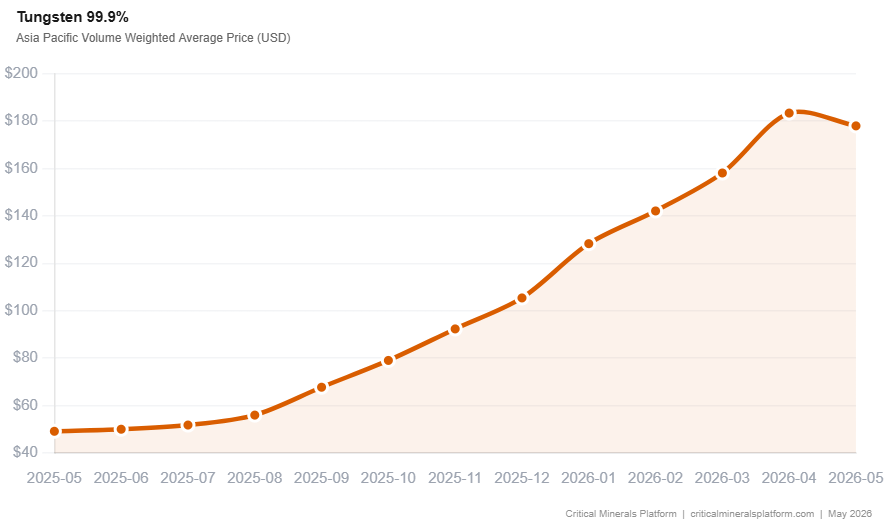

Europe, meanwhile, continued moving cautiously but steadily toward a more interventionist posture. Reuters reported that the European Union is considering stockpiling tungsten, rare earths, and gallium as part of its first coordinated strategic mineral reserve system. Brussels is also increasingly examining alternative pricing mechanisms to reduce dependence on opaque Chinese benchmark pricing systems.

These developments may ultimately prove highly significant. For years, Western critical mineral discussions focused almost exclusively on mining projects. Increasingly, governments are recognizing that resilience also requires inventory systems, transparent pricing mechanisms, metallization capacity, recycling infrastructure, and magnet manufacturing. In other words, the market is slowly beginning to understand that strategic minerals policy is fundamentally about industrial systems rather than simply resource extraction.

Several corporate developments reinforced this trend during the week. Reuters reported that Critical Metals Corp. (NASDAQ: CRML) signed a 15-year offtake agreement with REalloys Inc. (NASDAQ: ALOY) tied to concentrate production from the Tanbreez rare earth project in Greenland—one of the world’s largest known heavy rare earth deposits. The agreement included priority access to dysprosium and terbium-rich material, highlighting the increasing strategic importance of heavy rare earth supply chains outside China.

At the same time, debate continued surrounding the viability of several U.S.-backed rare earth initiatives. Bloomberg reported growing Pentagon concerns surrounding a proposed strategic financing package involving privately held ReElement Technologies Corporation, a rare earth refining and processing company affiliated with American Resources Corporation (NASDAQ: AREC). The episode once again illustrated the instability that can emerge when political urgency collides with the technical realities of rare earth separation economics, metallization capacity, and downstream magnet manufacturing execution.

Top of Form

Bottom of Form

This remains one of the defining characteristics of the current market cycle. Capital is now moving aggressively into critical minerals, but execution risk remains extraordinarily high. Building mines is difficult. Building separation facilities, metallization plants, alloy production, and magnet manufacturing ecosystems outside China is considerably more difficult.

The irony, perhaps, is that the geopolitical urgency surrounding critical minerals is finally forcing governments to acknowledge something the sector has understood for years: the problem was never simply geological scarcity. The real issue has always been industrial concentration.

That reality became clearer again this week.

China did not retreat from its strategic minerals position. It normalized it. Australia intensified its industrial and investment defenses. Europe moved closer toward stockpiling and pricing intervention. Washington accelerated industrial policy while simultaneously confronting the operational limits of its own supply chain ambitions.

And beneath it all, the market continued its gradual transition away from viewing critical minerals as a commodity story alone. Increasingly, this is becoming a story about industrial architecture, national resilience, manufacturing control, and geopolitical leverage.

The geology still matters. But the balance of power now increasingly resides in what happens after the rock leaves the ground.

Do you enjoy the Critical Minerals Report (CMR)?

Click here to become a Critical Minerals Institute member and get each edition delivered straight to your inbox.

InvestorNews Critical Minerals Institute (CMI) Directorial Headline Picks for the Past Week:

- May 22, 2026 – China squeezes Japan over rare earths in repeat of 2010 showdown (Source)

- May 21, 2026 – Pentagon Doubts Over Rare Earths Deal Provoke White House Clash (Source)

- May 21, 2026 – Miner Perpetua Resources secures $2.9 billion U.S. loan for Idaho gold, antimony project (Source)

- May 20, 2026 – EU shortlists tungsten, rare earths for first stockpile to curb reliance on China (Source)

- May 20, 2026 – China says rare earth controls lawful, will cooperate with US on ‘reasonable’ concerns (Source)

- May 20, 2026 – Australia’s Arafura approves $1.6 billion rare earths project (Source)

- May 20, 2026 – Europe must break China’s grip on rare earths pricing to spur investment, sector body says (Source)

- May 20, 2026 – China Set to Impose Mining Controls on Some Strategic Minerals (Source)

- May 18, 2026 – Critical Minerals Institute (CMI) Summit 5: Critical Minerals and the New Industrial Order (Source)

- May 18, 2026 – EU to force companies to buy components from non-Chinese suppliers, FT reports (Source)

- May 18, 2026 – Defence groups clamour to delay US ban on Chinese rare earth magnets (Source)

- May 17, 2026 – White House gets small rare earth win, but China’s export regime is here to stay (Source)

- May 17, 2026 – How Critical Minerals Are Reshaping America’s Industrial Future (Source)

- May 17, 2026 – Gina Rinehart’s Hancock Prospecting adds defense stocks to US portfolio (Source) –

- May 17, 2026 – Australia Orders Chinese Investors to Sell Rare Earth Stakes (Source)

- May 16, 2026 – Deal rush in rare earths as west seeks to loosen China’s grip (Source)

- May 14, 2026 – Pentagon’s ‘Deal Team Six’ Aims to Challenge China’s Grip on Rare Earth Power (Source)

InvestorNews.com Media Updates:

- May 20, 2026 – Jack-in-the-Stox: Quantum Critical Metals’ Quebec Gallium-Cesium Discovery https://bit.ly/4dAeCkl

- May 18, 2026 – Critical Minerals Institute (CMI) Summit 5: Critical Minerals and the New Industrial Order https://bit.ly/495bWtN

- May 17, 2026 – How Critical Minerals Are Reshaping America’s Industrial Future https://bit.ly/3Rfozwe

- May 14, 2026 – Lewis Black of Almonty Industries to Headline CMI Summit 5 with Stark Warning on the Critical Minerals Talent Crisis https://bit.ly/4nnIMfs

- May 13, 2026 – Feisal Somji of Sio Silica to Deliver Keynote at CMI Summit 5 on Securing North America’s Silica Supply Chain for the Fourth Industrial Revolution https://bit.ly/4f7gnIb

- May 12, 2026 – Pini Althaus to Deliver Keynote at CMI Summit 5 on U.S. Government Policy and Strategy in the Global Race for Critical Minerals https://bit.ly/4wa5Thf

- May 11, 2026 – “Twiggy” Pulling Out of Rare Earths? The Real Story Is Much Bigger. https://bit.ly/4wFmYjJ

- May 11, 2026 – Quantum Announces Participation in the Critical Minerals Institute (CMI) Summit https://bit.ly/3QT4N9M

InvestorNews.com News Release Updates:

- May 22, 2026 – Appia Announces Signing of Share Exchange Agreement with Ultra Rare Earth Inc. https://bit.ly/4a1byNa

- May 21, 2026 – West High Yield (W.H.Y.) Resources Ltd. Announces Private Placement Offering https://bit.ly/3PRP2zA

- May 21, 2026 – Appia Rare Earths & Uranium Corp. Qualifies for Third Consecutive Saskatchewan TMEI Grant of $70,910.87 https://bit.ly/3RTKTM1

- May 21, 2026 – Silver Bullet Mines Corp. Announces Adoption of Semi-Annual Reporting and Reliance on Quarterly Reporting Exemption Under Coordinated Blanket Order 51-933 https://bit.ly/3RqJdtm

- May 21, 2026 – Greenland Mines Signs Definitive Agreement to Acquire the Sarfartoq Neodymium-Praseodymium Rare Earths Project in Greenland https://bit.ly/4doLJJl

- May 21, 2026 – Spartan Metals Prepares for 2026 Drill and Exploration Program with Geophysics Survey at the Eagle Tungsten-Silver-Rubidium Project, Nevada https://bit.ly/4v1c9H0

- May 20, 2026 – Deep Sea Minerals Corp. Announces Proposed Share Split https://bit.ly/4nDsrDi

- May 20, 2026 – Neo Performance Materials Announces C$100 Million Bought Deal Treasury Offering of Common Shares https://bit.ly/4dmdFNT

- May 20, 2026 – Neo Partners with Greenland Mines to Advance Sarfartoq Rare Earth Project https://bit.ly/3RSbtoQ

- May 20, 2026 – Renforth Resources Inc. Adopts Semi-Annual Reporting https://bit.ly/4v0zyZ2

- May 20, 2026 – Homerun Resources Inc. Engages Minerali Industriali Engineering for Engineering and CAPEX Development of a Primary Silica Sand Processing Plant https://bit.ly/4nC4igl

- May 20, 2026 – Allied Critical Metals Announces Corporate Update and Operational Update https://bit.ly/4djCrya

- May 19, 2026 – West High Yield Resources Receives Draft Environmental Management Act Permit for Record Ridge Project https://bit.ly/4um8K5q

- May 19, 2026 – Nord Precious Metals Secures Original Technical Team to Update Historic Silver Tailings Resource at Gowganda https://bit.ly/3PfHDKi

- May 19, 2026 – Quantum Advances European Strategy Through EU Raw Materials Mechanism https://bit.ly/4wFy0Fr

- May 19, 2026 – Greenland Mines Brings Skaergaard to EIT RawMaterials Summit 2026 in Brussels https://bit.ly/4fsZIPs

- May 19, 2026 – Scandium Canada and ALPOMET Establish Collaboration Framework to Develop Scandium-Based Advanced Materials https://bit.ly/4eRr6Xe

- May 19, 2026 – Power Metallic Announces Expansion In the Kingdom of Saudi Arabia via Joint Venture With Amaar Mining https://bit.ly/497JRSB

- May 15, 2026 – Court approves convening of Scheme Meetings and Dispatch of Scheme Booklet https://bit.ly/439nJ6R

- May 15, 2026 – Drill Program Underway for Tungsten and Gold High Recoveries in Gold Metallurgy https://bit.ly/4dGB90d

- May 13, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Results at the Bald Hill Antimony Deposit Including Intersections of 26.9% Antimony (Sb) https://bit.ly/4noXXFb

- May 13, 2026 – Greenland Mines Ltd to Present at CMI Summit 5 as Western-Aligned PGM and Critical Minerals Developer https://bit.ly/4uIQi6X

- May 13, 2026 – American Rare Earths Appoints BDO as Auditor and Commences Nasdaq Listing Process https://bit.ly/4txfTi6

- May 13, 2026 – Power Metallic Partners with Ideon Technologies to Unlock Deep Discovery Potential at Nisk Lion Zone using Muon Tomography https://bit.ly/4dm9joH

- May 12, 2026 – Spartan Metals Announces Attendance at Investor Conferences https://bit.ly/4dloMFF

- May 12, 2026 – Homerun Resources Inc. Announces Positive Bankable Feasibility Study on Solar Glass Manufacturing Plant in Brazil, Confirming Strong Economics and Strategic First-Mover Position in the Americas https://bit.ly/4nrc10X

- May 12, 2026 – Neo Performance Materials Reports First Quarter 2026 Results https://bit.ly/4u9wda6

- May 12, 2026 – Defense Metals Commences Pilot Flotation Test Program at SGS Lakefield for the Wicheeda Rare Earth Project https://bit.ly/4dliENq

- May 12, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Drill Results up to 13.9% Antimony (Sb) in Stibnite Bearing Core https://bit.ly/4323kAx

About the Critical Minerals Institute (CMI)

The Critical Minerals Institute (CMI) is a global brain trust for the critical minerals’ economy, serving as a hub that connects companies, capital markets, and policymakers. Through CMI Masterclasses, the weekly Critical Minerals Report (CMR), bespoke research, and board-level advisory services, CMI delivers actionable intelligence spanning exploration finance, supply chains, and geopolitics. For more information on the CMI, go to Critical Minerals Institute (CMI).