Managing the War Economy

Let’s face it, the West has not had to manage a war economy since 1945. The Korean War provided some stresses, but all the subsequent conflagrations, even ones that seemed serious at the time like Vietnam or Afghanistan or Iraq, were small beer compared to the shockwaves, both military and economic, emanating from the current conflict.

Frankly, despite all the huffing and puffing since the First Rare Earth crisis of 2009-11, the West has failed totally to gird its loins for the struggle ahead and seems moreover to have adopted the rules of a German nudist colony and “let it all hang out” rather than do something constructive to underpin the rhetoric, or cover their inadequacies.

Despite the fact that its now well over a year since China brought in dual-use exports bans on a number of key military elements (Tungsten, Antimony etc) and several years since Rare Earths, Gallium and Germanium were squeezed by Peking, the West has seemingly not been able to get out of its own way on the issue of upping production and the US is worst of the lot. There has not been one teaspoon of Tungsten or Antimony mined in the US over the last 12 months!

While its fashionable in Washington to refer to Europe as the Sick Man of Europe (to use the old trope levelled at the Ottoman Empire) the EU has a quantum more Tungsten production than the US has managed. The EU has way more Rare Earth processing capability than the US with Neo Performance Materials Inc.’s (TSX: NEO | OTCQX: NOPMF) plant at Silmet in Estonia and the sometime processing facility that was Rhodia STER/Solvay S.A. (Euronext Brussels: SOLB) at La Rochelle in France.

War is good for metals, or so goes the theory. But is it? The main materiel consumed so far is just that which goes into the drones or the missiles, which are flitting back and forth. The total tonnage of shipping sunk (naval or commercial is small). If iron ore is the prime military metal (in terms of size) then the war so far is a non-starter. This is similarly the case for aluminium (except the Qataris potlines which have “set”). Copper, nickel and zinc scarcely figure in this “shooting war”.

At the end of the first week of March, a gathering of the military-industrial complex (the same one Eisenhower warned against) took place at the White House. In attendance were the chief executives of RTX Corporation (NYSE: RTX), Lockheed Martin Corporation (NYSE: LMT), The Boeing Company (NYSE: BA), Northrop Grumman Corporation (NYSE: NOC), BAE Systems plc (LSE: BA.), L3Harris Technologies, Inc. (NYSE: LHX) and Honeywell International Inc. (NASDAQ: HON). This was designed to ginger up a production surge from these worthies.

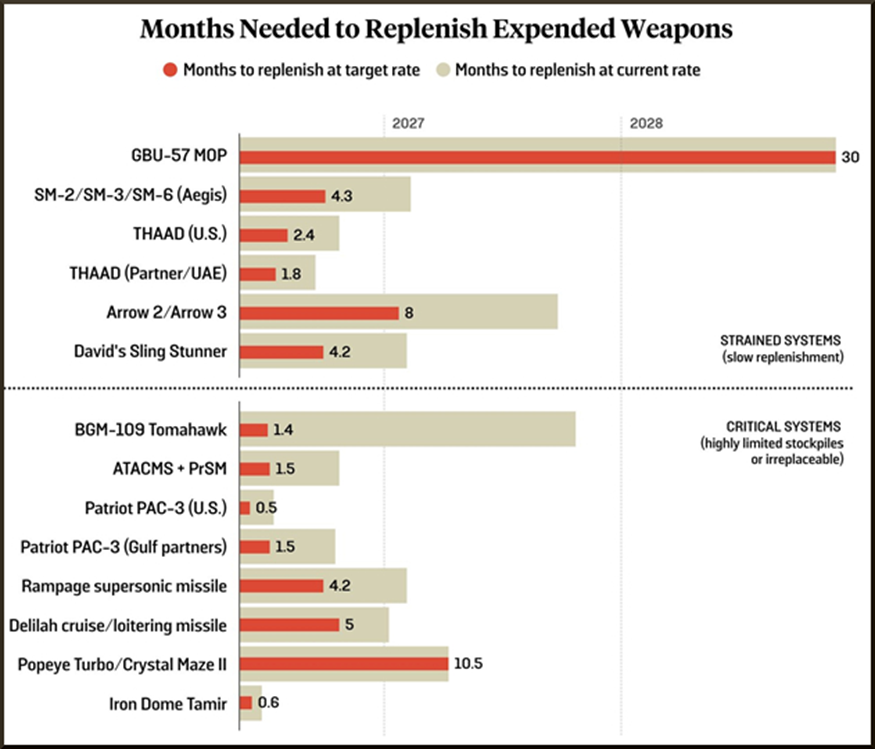

The table on the following page, crafted by the Payne Institute for Public Policy in Golden, Colorado, shows the months to replenish critical and strained weapons systems.

Source: Payne Institute

“Strained” is a new word for the promotorial classes, but we are sure it will get some traction as no conflict goes unturned as a source of inspired marketing. Even we can definitely see that a case could be made for Tungsten, Antimony and even Tin being “strained” at the current time by a number of factors, both military and commercial and both user-side and producer-side.

The Washington pow-wow was a belated effort to jazz up the “complex” and put pedal to the metal on war production. However, this was held on Day Six of Operation Epic Failure which was supposed to be over by Day Two or Day Four, so why should any of these execs have their weekday jobs disturbed by anything beyond the ringing of their tills? It was all supposed to have been over by then, with them carrying on their leisurely and highly remunerative creation of expensive toys.

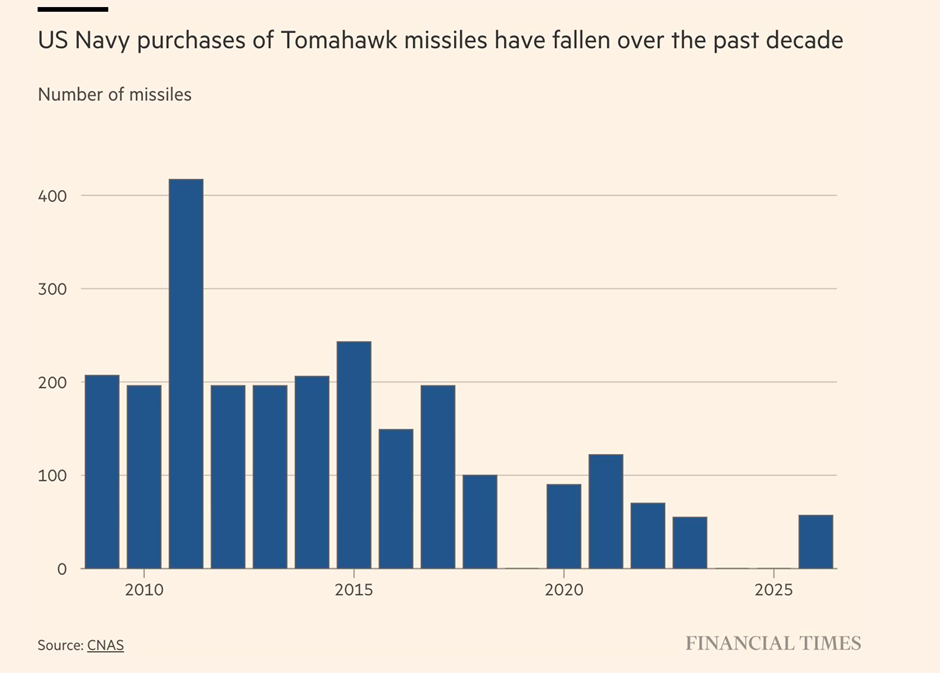

The White House wants immediate results, but even they should know that even Atlantic City was not built in a day. It takes planning and order flow. The chart below shows how US orders for Tomahawk missiles have faded over the last decade and yet Washington is now exhorting the military-industrial complex to “get their skates on”.

Source: CNAS/Financial Times

Reports stated that it was not immediately clear whether the meeting resulted in any new agreements to boost production beyond those previously announced by the Pentagon since the beginning of the year. That a follow-on meeting was going to be in two months, pretty well signified the “urgency” of the matter.

Apparently, exhortations for Stakhanovite effort directed to critical metals/minerals companies were also issued. Had MP Materials Corp. (NYSE: MP) and USA Rare Earth, Inc. (NASDAQ: USAR) (singular) also been summoned? It is not immediately clear what additional production capacity MP Materials could realistically bring online in the near term. Meanwhile, USA Rare Earth continues the longer process of building out its domestic magnet and processing ambitions. Policy urgency is one thing; materially increasing rare earth production in short order is quite another.

Almonty Industries Inc. (NASDAQ: ALM | TSX: AII | ASX: AII) is leading the charge on (real) Tungsten production but its game changing new mine in South Korea is located in a jurisdiction where the US has just pulled out the THAAD systems to shift them to protect Israel. Sigh…. How much Tungsten does Israel produce?

War is basically bad for business for all except the very few. Those who saw (supposed) streamlined planning/permitting approvals and highly selective largesse towards a couple of critical metals stories as being a Brave New World are in the process of being disabused daily as they watch the unfolding disaster movie.