Seven consecutive years of gold production growth?

Karora Resources is growing to become the next 200,000 ounce gold producer

Gold had a good year in 2023 up 15% and is currently trading at US$2,028/ounce. The gold sector looks like it will have a strong 2024 as the macro backdrop for gold improves. Here are four reasons why:

- A series of three interest rate cuts in the USA is forecast for 2024, which may also lead to a weaker U.S. dollar (“USD”). Lower rates and a lower USD are good for the gold price.

- Growing geopolitical uncertainty – The Ukraine-Russia war continues, the Israel-Hamas war may spread to nearby Middle East regions as we saw recently with the U.S. response to the Red Sea shipping attacks by Houthis against Israeli ships, etc.

- The U.S. Presidential election on November 5, 2024. Any instability as we saw after Trump lost the last election may result in a flight to safe assets.

- According to Sprott Research – “Gold mining stock valuations are the lowest in 25 years”.

For those investors looking at a growing mid tier gold miner that keeps on delivering on their promises then today’s company will be right up your alley.

Karora Resources Inc.

Karora Resources Inc. (TSX: KRR | OTCQX: KRRGF) (“Karora”) is a Canadian gold mining company with growing gold operations ~60 kms from Kalgoorlie, in Western Australia. Karora’s 100% owned assets include several gold mines (Beta Hunt underground Mine, Higginsville Gold Operations (“HGO”), Spargos Gold Mine), and their two gold mills (Higginsville Mill, Lakewood Mill). Karora produced 160,492 gold ounces in 2023 and has their next major target set at 200,000 ounces pa.

Karora’s consolidated contained gold resource across all operations is M&I Resource of 3.189m Oz @ 2.0 g/t Au and an Inferred Resource of 1.538m Oz @ 2.4g/t Au.

Location map showing Karora Resources 1,900 sq. km of tenements, 3 key gold mines, and 2 Mills

Source: Karora Resources company presentation

Karora Resources under promises and over delivers

As announced on January 15, 2024, Karora produced a record 160,492 ounces of gold for 2023 compared to their guidance range of 145,000 – 160,000 ounces. Karora Chairman & CEO, Paul Andre Hue, commented:

“I am extremely pleased to announce Karora’s seventh consecutive year of production growth. We produced a record 160,492 ounces of gold for 2023, exceeding 2022 production by over 26,000 ounces and beating the high end of our full year 2023 guidance range of 145,000 – 160,000 ounces. Gold production in the fourth quarter was a very strong 40,295 ounces, the second highest quarterly result on record.“

Seven consecutive years of production growth – Wow, that’s impressive.

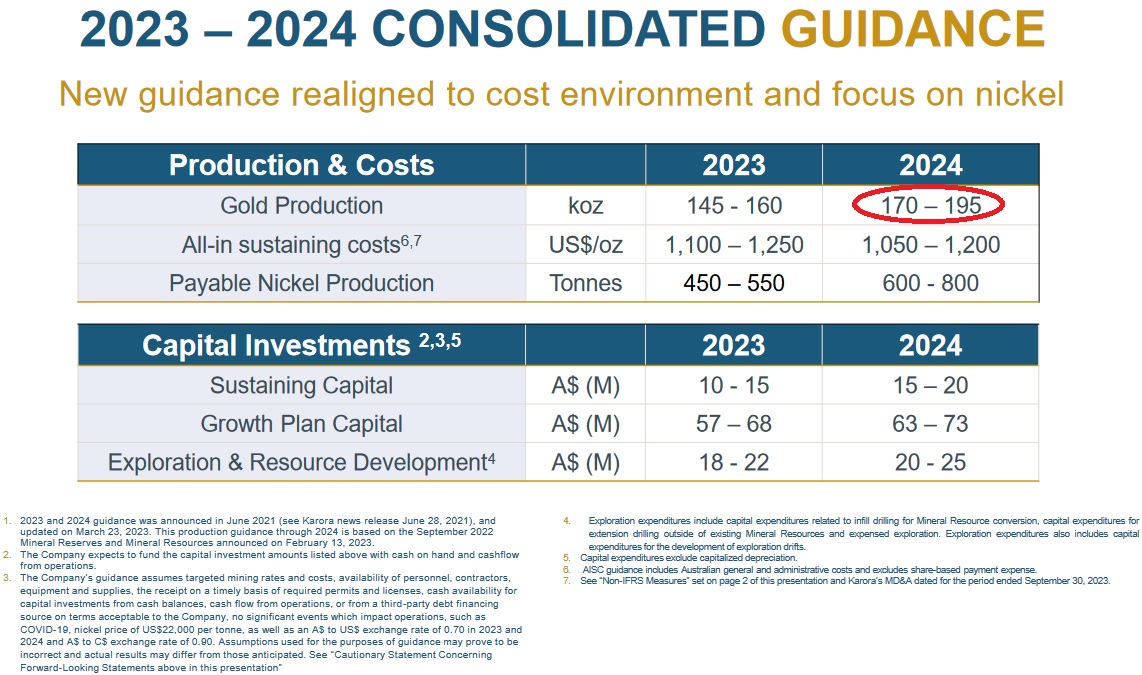

The news only gets better from Karora as they are guiding to achieve 170,000-195,000 gold ounces in 2024 at a lower AISC of US$1,050 – 1,200/ounce.

Karora’s 2024 guidance, if achieved, would make them an almost 200,000 ounce pa gold producer

Source: Karora Resources overview

A key point to note from the chart above is point 2 – “The Company expects to fund the capital investment amounts listed above with cash on hand and cash flow from operations.” Karora currently has a very robust balance sheet with C$82.5 million in cash as of December 31, 2023.

Another key plus for Karora is that they are starting to increase their nickel by-product production. As this grows it helps Karora maintain or reduce their All In Sustaining Costs (“AISCs”).

Closing remarks

The macro set up for 2024 certainly looks very favorable for gold. If we get declining interest rates and a weaker USD, then the gold price is likely to move higher in USD terms. If global geopolitical tensions worsen then that will favor the safe haven of gold.

Karora Resources is a standout small gold miner growing steadily to becoming a mid-tier 200,000 ounce pa gold producer at a very reasonable AISC near US$1,000/ounce. Management continues to deliver results at or above expectations. Finally, sovereign risk is extremely low with Western Australia being a tier one mining jurisdiction.

Karora Resources trades on a market cap of C$771 million and a 2024 PE of 11.9.