Critical Minerals Report (07.05.2026): The Hunt for Industrial Expertise Is On.

The past fourteen days materially advanced the shift of critical minerals from a supply-chain issue into a policy-and-security file. China broadened export controls across both Japanese and U.S. entities, strengthened enforcement against smuggling, and continued to frame licensing as a national-security tool; the G7 answered with a new coordination platform, common diversification targets, and more explicit stockpiling language; and both Washington and Ottawa tied mineral security more tightly to nuclear, defense procurement, and midstream processing capacity. At the same time, the most consequential corporate moves were not new discoveries but integration plays: Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) agreed to buy Vacuumschmelze GmbH & Co. KG for an equity value of about US$1.9 billion, while the legal fight between MP Materials Corp. (NYSE: MP) and USA Rare Earth, Inc. (Nasdaq: USAR) made clear that magnets, alloying, and process know-how are now central competitive battlegrounds, not side issues. The same pattern appeared in lithium, where battery-storage demand became a larger commercial driver, and in tungsten, where Almonty Industries Inc. (TSX: AII | ASX: AII) and the Sangdong mine in South Korea moved further into the strategic mainstream.

What mattered most over the fortnight was where policy concentrated. Governments moved faster on loans, quotas, stockpiles, trade rules, and export licensing than on mine approvals. The U.S. announced US$17.5 billion in conditional nuclear-supply-chain loans intended to accelerate ten large reactors, Canada laid out a plan for up to ten new reactors by 2040, the Democratic Republic of Congo tightened cobalt quota enforcement while signalling a broader western rebalancing, and the European Union stepped up its courtship of Brazil with an offer centred on processing and industrial cooperation rather than simple raw-material extraction. In that sense, the market signal from the last two weeks was unmistakable: the bottlenecks that now matter most sit in the midstream and downstream, especially refining, separation, metallisation, magnet manufacturing, and nuclear-fuel services.

Welcome to this week’s Critical Minerals Report (CMR), prepared with the valued support of Critical Minerals Institute (CMI) Co-Chairs Melissa Sanderson and Jack Lifton, together with our Perth-based data intelligence partners, the Critical Minerals Platform (CMP).

China once again dominated the week’s strategic developments. Beijing expanded export controls affecting 40 Japanese entities, imposed additional restrictions on selected U.S. companies, added American entities to its export control list, strengthened enforcement against critical mineral smuggling through a new whistleblower hotline, and detained two Japanese nationals over alleged rare earth smuggling. These actions span the entire critical minerals supply chain—from mining and processing to exports and technology transfer—and suggest that export licensing is becoming an increasingly permanent element of China’s industrial policy rather than a temporary trade measure.

China extended the same approach to U.S. counterparties on June 22nd, when it placed 10 American entities, including MP Materials Corp. (NYSE: MP) and USA Rare Earth, Inc. (Nasdaq: USAR), on its export-control list and separately barred Chinese public buyers from procuring goods from 46 U.S. companies. Reuters reported that the move tightened earlier rules that had required licenses into an outright ban on dual-use exports to the named firms, while the Financial Times described the measures as part of a retaliatory cycle that followed U.S. action against Chinese companies alleged to support the Chinese military. The practical commercial effect on MP Materials and USA Rare Earth may be limited, but the strategic point is harder to dismiss: China is now willing to name, target and publicly signal against companies central to the West’s rare earth build-out. That aligns with a June survey by the U.S.-China Business Council, which found some critical minerals had become “nearly unobtainable” from China despite the two sides’ earlier commitments to ease restrictions.

The G7 responded by moving its critical minerals language closer to operational policy. Leaders agreed on a new alliance and crisis platform, said they would work to reduce dependence on any single non-G7 supplier for rare earths and permanent magnets to below 60% by 2030, and set an eventual 50% goal “as soon as possible.” Reuters reported that roughly €64 billion had already been announced across 195 projects since early 2026, while China’s foreign ministry answered within a day by defending its export controls and warning against “small cliques.” Beijing simultaneously signalled its alternative external strategy when Foreign Minister Wang Yi called on BRICS countries to strengthen cooperation on strategic mineral resources. The resulting picture is not one of retreat from global markets, but of parallel bloc-building around the same materials.

North American coordination remained strategically necessary but politically uneven. On July 1st, the Trump administration declined to renew the United States-Mexico-Canada Agreement in its current form, starting the sunset review clock while leaving the pact in force and reopening negotiations over rules of origin, trade balances and broader manufacturing policy. North American trade architecture still underpins about US$1.6 trillion in annual trilateral trade, which is precisely why the decision matters for critical minerals: the United States cannot realistically build continental supply chains for uranium, rare earths, tungsten, graphite, nickel and potash without Canada, even as Washington’s trade posture has become more transactional. Ottawa has continued to push for a multilateral “buyers’ club” approach to critical minerals and, in the past week, extended that outward by backing a Greenland molybdenum project with C$7 million in grants. That combination—trade uncertainty on the one hand, mineral-security partnership on the other—captures the current Canada-U.S. relationship more accurately than either rhetoric or communiqués alone.

These issues are explored in greater depth in the latest edition of the Critical Minerals Report bi-monthly podcast, which Jack Lifton, Melissa Sanderson and I recorded today.

The European Union spent the same period trying to distinguish its offer to Brazil from the more explicit resource-security approaches taken by Washington and Beijing. EU Commissioner Jozef Síkela pitched Brazil as the bloc’s “most strategic” Latin American partner for critical minerals, visited rare earth developments in Minas Gerais, and framed Brussels’ offer around technology transfer, local processing, refining capacity, jobs and environmental standards. That matters because Brazil holds the world’s second-largest rare earth reserves and is rapidly becoming one of the few jurisdictions outside Asia with real optionality in heavy rare earths. The U.S. has already moved to secure offtake influence through Development Finance Corporation support for Serra Verde, but Europe’s message to Brasília was that supply diversification will be more durable if downstream value is built in-country rather than extracted and shipped out as feedstock [Source].

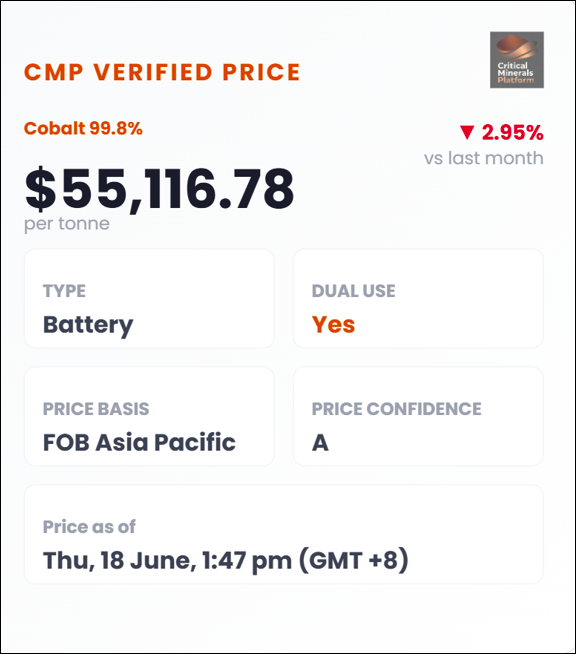

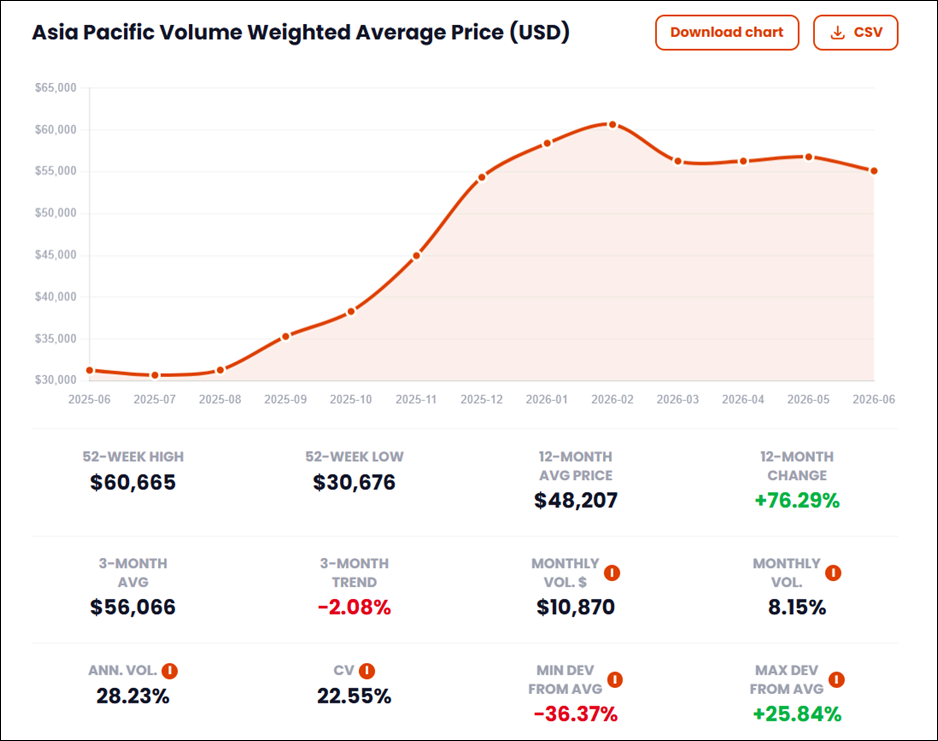

The Democratic Republic of Congo tightened its grip on cobalt again, and the market noticed. Reuters reported on June 29th that unused first-half export quotas would be withdrawn and reassigned to a state-controlled entity, then reported on July 3rd that an administrative glitch could strand roughly 20,000 tonnes of cobalt exports worth about US$1.1 billion before the July 5 deadline. The same Reuters coverage said ARECOMS has imposed a 96,600-tonne annual cap for 2026 and 2027, while cobalt prices have risen about 160% since February 2025 to US$57,320 a tonne (CriticalMineralsPlatform.com). Kinshasa is using tighter market management to raise prices, promote local value addition, and reduce exclusive dependence on Chinese operators by opening more space for Western infrastructure and financing, including the Lobito corridor and new U.S.-linked cobalt processing relationships. For battery and defense buyers alike, the DRC is the active rule-maker (Source).

The most consequential corporate transaction of the fortnight was Energy Fuels Inc.’s agreement to acquire Vacuumschmelze GmbH & Co. KG for an equity value of about US$1.9 billion. This deal is for US$718 million in cash and 65.853 million newly issued Energy Fuels shares, leaving seller Ara Partners with a 19.9% stake. The deal followed an earlier announcement on June 18th that Energy Fuels had signed a US$725 million conditional loan commitment with the U.S. Office of Strategic Capital to expand domestic rare earth separation and metallization. Read together, the two moves show how quickly the logic of Western rare earth strategy has shifted from mine development to integrated control of separation, metals, alloys and finished magnets. The acquisition also gives Energy Fuels a route into VAC’s century-old industrial base, its customer relationships and its patent estate rather than forcing the company to build each capability from first principles.

The legal dispute between MP Materials Corp. (NYSE: MP) and USA Rare Earth, Inc. (Nasdaq: USAR) sharpened the same point from the opposite direction, claiming an alleged misappropriation of proprietary magnet technology. USA Rare Earth denied the allegations and the Wall Street Journal stepped in and described the case as a fight over grain-boundary-diffusion technology and, more broadly, over who becomes America’s rare earth champion. The commercial facts around both companies underline why the lawsuit matters: each has received substantial U.S. policy support, each is racing toward a mine-to-magnet model, and both were named by China in its June 22nd export-control response. In other words, the dispute is not peripheral litigation; it is evidence that the strategic scarcity in rare earths now lies as much in process knowledge and industrial execution as in ore.

Australia kept pushing public capital into downstream rare-earth capacity. Iluka Resources Limited (ASX: ILU) secured a non-recourse A$1.65 billion loan from Canberra for the Eneabba rare-earth refinery, a development described as one of the clearest signs yet that allied governments are prepared to support processing assets directly where markets alone will not. Lynas Rare Earths Limited (ASX: LYC) remains the largest producer outside China, but its Malaysian operations also show why permitting and licence conditions remain part of the sector’s strategic equation: Malaysia renewed Lynas’s licence for ten years in March, while requiring the company to stop producing radioactive waste by 2031 and to neutralise any legacy residue under tighter conditions.

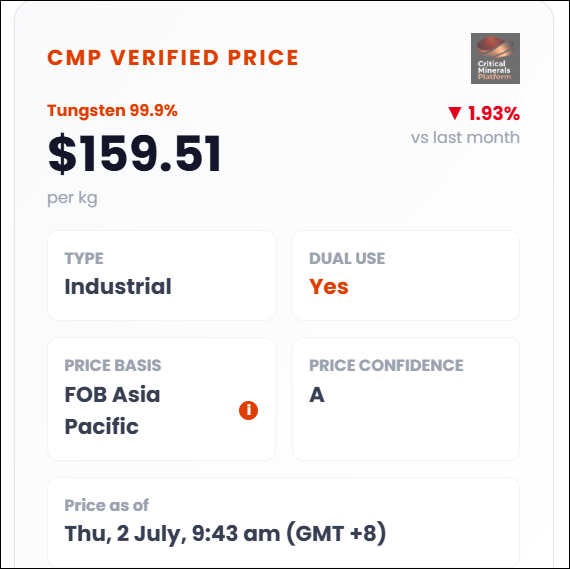

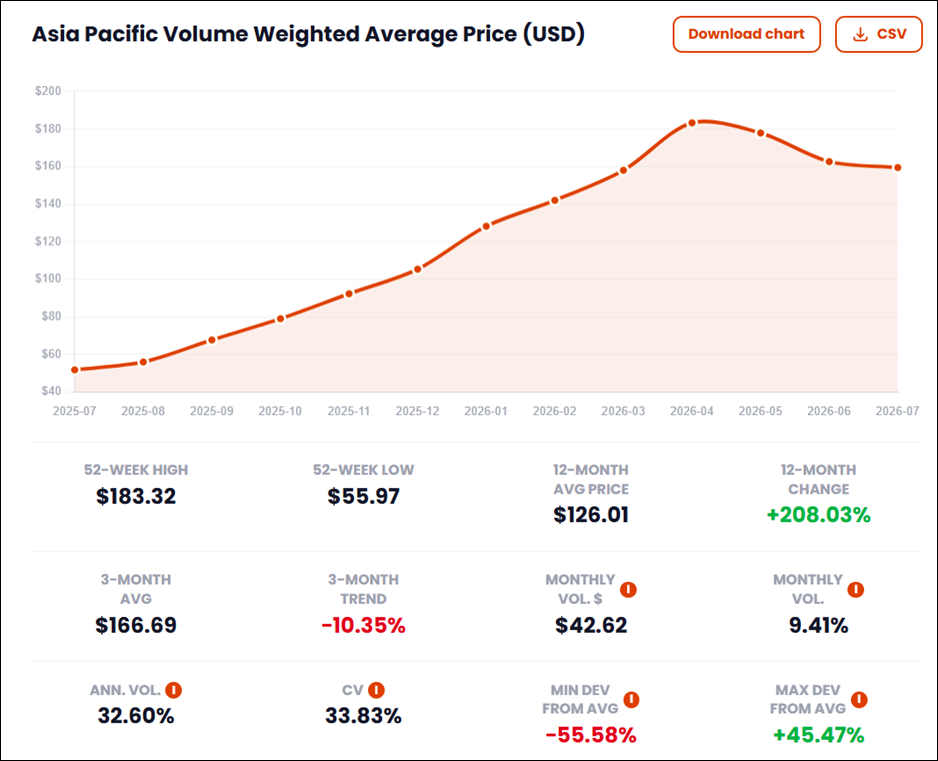

Tungsten moved materially closer to the center of the defense-supply discussion. China controls more than 80% of the global tungsten market, while the West’s most advanced near-term non-Chinese response is the Sangdong mine in South Korea, where Almonty Industries Inc. (NASDAQ: ALM; TSX: AII; ASX: AII) has been commissioning phase-one production, with first output committed to Plansee’s U.S. arm under a floor-price arrangement. Current ammonium paratungstate prices remain well above the contractual floor price, underscoring how strategic security and market support are now being written directly into tungsten offtake structures. That geopolitical elevation was echoed in the source material, which highlighted a July 1 New York Times feature on Sangdong and included official company updates from American Tungsten Corp. (TSXV: TUNG | OTCQB: TUNGF), Spartan Metals Corp. (TSXV: W | OTCQB: SPRMF; FSE: J03), and Fox Tungsten Ltd. (TSXV: FOXT). In those releases, American Tungsten reported 125 feet of tungsten-silver mineralization, Spartan reported both skarn confirmation at its Eagle Project in Nevada and historic drilling validation at Victorio in New Mexico, and Fox Tungsten announced a 20,000-metre drill program.

Lithium producers spent the week telling investors that the market’s second demand engine is now large enough to matter in its own right. Lithium demand for stationary battery storage is growing at about 40% a year, while lithium prices have more than tripled since 2025. Producers such as Albemarle Corporation (NYSE: ALB), Rio Tinto plc/Rio Tinto Limited (LSE: RIO; ASX: RIO; NYSE: RIO), and ioneer Ltd (ASX: INR) are explicitly rebalancing their demand assumptions toward grid-scale energy storage. Rio expects lithium to become its fastest-growing business, targeting annual production of 200,000 tonnes by 2028, while Contemporary Amperex Technology Co., Limited (SZSE: 300750), better known as CATL, expects energy storage to grow from about one-quarter of current sales to half of global sales by 2030. In Australia, The Australian reported that Gina Rinehart’s Hancock Prospecting Pty Ltd, together with Sociedad Química y Minera de Chile S.A. (NYSE: SQM), plans to develop the Andover mine in Western Australia with output of up to 1.1 million tonnes of concentrate annually over a 30-year mine life. The combined message is less about a single price cycle than about demand broadening beyond electric vehicles into electricity grids, renewable energy, AI-driven data centres, and broader industrial resilience.

Nuclear policy and defence procurement moved in parallel. On June 23rd, the U.S. Department of Energy announced US$17.5 billion in conditional loans aimed at accelerating ten large AP1000 reactors, and Reuters reported that Secretary Chris Wright said the programme could bring the 2030 build target forward by three years. On June 22nd, Canada laid out a strategy to have up to 10 new large reactors built or under development by 2040, with two under construction by 2035; Reuters noted that nuclear already supplies about 13% of Canadian electricity and that Canada is the world’s second-largest uranium producer. The supporting fuel-cycle build-out is also real rather than rhetorical: Urenco said in June that it would expand the only U.S. commercial uranium-enrichment plant by nearly 50%. Meanwhile, the White House convened munitions makers over depleted weapons stockpiles, and the U.S. Army selected Titan Mining Corporation (TSX: TI) and REalloys Inc. (Nasdaq: ALOY) to develop critical mineral processing sites. The immediate implication for uranium is straightforward, but the broader implication for critical minerals is larger: defense, power reliability and industrial policy are now sharing the same procurement language.

If one conclusion emerges from this week’s developments, it is that the critical minerals race is becoming less about discovering resources and more about building industrial capability. Across rare earths, lithium, tungsten, uranium, and battery materials, the competitive advantage is shifting toward processing, manufacturing, customer qualification, secure supply chains, and execution. That same theme runs through two timely commentaries published today by CMI Co-Chair Jack Lifton. In Let’s Pretend: Subject Matter Illiteracy and the Rare Earth Industry, Lifton draws on Stephen Hawking’s observation that “The greatest enemy of knowledge is not ignorance, it is the illusion of knowledge,” arguing that too much of today’s critical minerals debate remains detached from the practical realities of industrial production. His companion piece, France Is Rebuilding a Rare Earth Industry. North America Is Still Selling the Story, reaches a similar conclusion from a different perspective: countries that succeed will be those that build complete industrial ecosystems rather than relying on deposits, announcements, or political rhetoric alone. Together, those essays reinforce the central message of this week’s Critical Minerals Report: the global competition for critical minerals has entered a new phase in which industrial competence, operational experience, and integrated supply chains are becoming more valuable than geology itself.

Enjoy the Critical Minerals Report (CMR)?

Join the Critical Minerals Institute (CMI) and receive the CMR directly in your inbox each week.

To learn more about CMI membership benefits, visit CriticalMineralsInstitute.com.

For premium pricing data, market intelligence, and critical minerals insights, visit CriticalMineralsPlatform.com.

Get your first month free and save 20% with promo code CMI2026.

InvestorNews Critical Minerals Institute (CMI) Directorial Headline Picks for the Past Week:

- July 01, 2026 – The South Korean Mine at the Center of America’s Tungsten Push (Source)

- July 01, 2026 – U.S. Declines to Renew Trade Pact with Mexico and Canada (Source)

- June 30, 2026 – China imposes export controls on 40 Japanese entities as tensions with Tokyo rise (Source)

- June 26, 2026 – EU pitches Brazil a ‘more beneficial’ rare earths deal than US or China (Source)

- June 25, 2026 – ‘Looming dangers’ under China-US ties: AI and rare earths reveal a fragile floor (Source)

- June 24, 2026 – The US needs Canada to win the critical minerals race (Source)

- June 24, 2026 – Lithium producers bet on battery storage as demand shifts beyond EVs (Source)

- June 24, 2026 – China plans whistleblower hotline to help it catch critical mineral smugglers (Source)

- June 24, 2026 – Congo pivots westward under cover of cobalt controls (Source)

- June 24, 2026 – China detains two Japanese nationals over alleged rare earth smuggling (Source)

- June 24, 2026 – As the G7 moves to cut reliance on China, Beijing is turning to BRICS for critical minerals (Source)

- June 23, 2026 – Trump administration to loan $17 billion to speed deployment of 10 big nuclear reactors in U.S. (Source)

- June 23, 2026 – Energy Fuels Announces Definitive Agreement to Acquire VAC for $1.9 Billion Equity Value (Source)

- June 23, 2026 – Australia’s $1.15 billion rare earths bet strengthens market for Africa’s next major mine (Source)

- June 22, 2026 – USA Rare Earth Rebuts MP Materials Suit as Rivalry Deepens (Source)

- June 22, 2026 – China restricts trading with some US rare earth companies (Source)

- June 22, 2026 – China adds 10 US entities to export control list following US expansion of ‘China military-industrial entity’ list (Source)

- June 22, 2026 – Energy minister plans ‘nuclear renaissance’ with up to 10 reactors built by 2040 (Source)

- June 22, 2026 – China Tightens Rare-Earth Grip on U.S. Firms, Threatening Trade Clash (Source)

- June 22, 2026 – Gina Rinehart’s new lithium mine to rival world’s biggest producers (Source)

- June 22, 2026 – Malaysian authorities reportedly block Lynas Rare Earths refinery expansion (Source)

- June 22, 2026 – White House set to host weapons makers amid stockpile worry (Source)

- June 22, 2026 – EU courts Brazil as strategic partner in global race for critical minerals (Source)

InvestorNews.com Media Updates:

- July 01, 2026 – Why OEMs, Not Governments, Will Decide America’s Critical Minerals Future https://bit.ly/4oVHvwK

- July 01, 2026 – Jack-in-the-Stox: In Rare Earths, Bigger Isn’t Always Better https://bit.ly/4eD0Yim

- June 29, 2026 – Rebuilding the Rare Earth Industrial Base, the Role of Government https://bit.ly/4aw5jS2

- June 25, 2026 – Private Capital, Not Government Funding, Is the Key to Securing Rare Earth Magnet Supply Chains https://bit.ly/3SwR6xU

- June 24, 2026 – Jack-in-the-Stox: Iluka Resources (ASX: ILU) — A Lesson in Rare Earth Execution https://bit.ly/4xQUZOw

- June 23, 2026 – Energy Fuels and the Emergence of a Credible Magnet Competitor https://bit.ly/4ahyMis

- June 22, 2026 – Critical Minerals Institute Announces CMI Summit 6 at Toronto’s Fairmont Royal York and Appoints Constantine Karayannopoulos to Board of Directors https://bit.ly/4ah8LzM

InvestorNews (YouTube) Interview Updates:

- July 02, 2026 – How Defense Metals Is Positioning Wicheeda as North America’s Next Rare Earths Producer https://youtu.be/vZWYSlART0s

- June 29, 2026 – The Next Critical Mineral: How Homerun Resources Is Building the Infrastructure for AI, Solar and Advanced Manufacturing https://youtu.be/4ZVglK85G34

- June 23, 2026 – CMR Special Podcast: Critical Minerals, China, and the Limits of G7 Cooperation https://youtu.be/pCwGk0pGgDk

InvestorNews.com News Release Updates:

- June 30, 2026 – AnorTech and Greenland Mines Close Strategic Share Exchange Transaction https://bit.ly/4giUvKC

- June 30, 2026 – Nord Precious Metals Announces Clarification to Investor Relations Agreements https://bit.ly/4gPvff9

- June 30, 2026 – Allied Critical Metals Announces Conditional Approval to List on the TSX Venture Exchange https://bit.ly/4oYVfqH

- June 30, 2026 – American Tungsten Corp. Adjourns Annual General and Special Meeting https://bit.ly/4ePvCUw

- June 30, 2026 – Spartan Metals Identifies 537 Feet (163.7 Meters) 0.23% WO3Eq or 0.31% MoEq During Historic Drilling Validation at Its Victorio Tungsten-Molybdenum Project, New Mexico https://bit.ly/447FuEc

- June 30, 2026 – Element One Invited to Help Shape British Columbia’s Hydrogen Strategy https://bit.ly/4vJgkYw

- June 29, 2026 – Nord Precious Metals Announces OTCQB US Symbol Change to “NPMMF” https://bit.ly/4geu2hh

- June 29, 2026 – Renforth Resources Visually Observes Mineralization in Channel Cutting of Diorites and Felsites in Open Pit Footprint at Parbec Gold Deposit https://bit.ly/4au2dOj

- June 29, 2026 – Oreterra Completes Airborne Geophysical Survey of the Kinkaid Cu-Au-Ag Project, Nevada, Identifies Significant New Porphyry Target https://bit.ly/3SSwC2J

- June 29, 2026 – Appia Identifies Three High-Priority Drill Targets at Its Otherside Uranium Property Similar to the McArthur River Ingress/Egress Deposit Model https://bit.ly/4oRFr8Y

- June 29, 2026 – Nord Precious Metals Further Extends Castle East Robinson Zone with 13,620 g/t Silver and 1.84% Cobalt over 0.6m, Including 25,803 g/t Silver (752.7 oz/ton) and 3.60% Cobalt over 0.30m https://bit.ly/4vE4Wgw

- June 29, 2026 – Scandium Canada Acquires and Rebrands Ferreol Technologies as Scalium+, Its New Alloy Commercialization Subsidiary https://bit.ly/4v1MJbO

- June 29, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Reports Gold Assays Up To 1.88 Grams per Tonne (g/t) Gold Over 4.85 Meters from Drill Core Samples in the Main Zone at Bald Hill Antimony Project https://bit.ly/4vGCafo

- June 26, 2026 – Western Uranium & Vanadium Announces Results of 2026 AGM https://bit.ly/4v6nlSf

- June 26, 2026 – Deep Sea Minerals Corp. Responds to Reuters Headline and Clarifies Status of NOAA Exploration Application https://bit.ly/4vCUJB0

- June 25, 2026 – Greenland Mines Concludes Three-Day Technical Workshop to Define and Advance Next Phase of Skaergaard Gold and Critical Metals Project Development https://bit.ly/4g6ekF0

- June 25, 2026 – Fox Tungsten Announces Start of 20,000m Drill Program https://bit.ly/4xNvfCn

- June 25, 2026 – Quantum Critical Metals Appoints Critical Minerals Institute (CMI) Founder Tracy Hughes to Board of Directors https://bit.ly/4v6CfYQ

- June 25, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Reports Assays up to 20.5% Antimony from Trench Grab Samples in the Central Zone at Bald Hill Antimony Project https://bit.ly/4vFqObt

- June 25, 2026 – Spartan Metals Reports Significant Silver-Antimony-Copper Assays with Grades up to 1,927 g/t Ag, 0.67% Sb, and 1.83% Cu from Past Producing Antelope Mine, Nevada https://bit.ly/4g5Oa5g

- June 25, 2026 – Power Metallic Announces Appointment of Christopher Beal as Vice President of Operations https://bit.ly/4vyV5J4

- June 25, 2026 – Pre-Feasibility Study and maiden Ore Reserve confirm Koppamurra as a compelling project https://bit.ly/43QVVol

- June 25, 2026 – Maiden Ore Reserve positions Koppamurra for development https://bit.ly/4wu0iSD

- June 25, 2026 – Koppamurra Pre-Feasibility Study Investor Webinar https://bit.ly/4uWvo3Q

- June 24, 2026 – West High Yield Resources Receives BC Ministry of Transportation and Transit Access Permit for Record Ridge Magnesium Project and Announces Second Tranche Closing of Private Placement https://bit.ly/3T0SetL

- June 24, 2026 – American Rare Earths (ARE) to Appoint Veteran Miner Matthew Gili as Non-Executive Director https://bit.ly/4uYLtWX

- June 23, 2026 – Voyageur Pharmaceuticals Engages Fluor to Advance Feasibility Studies for Iodine Production and Integrated Contrast Drug Manufacturing Facility https://bit.ly/44t6FcC

- June 23, 2026 – Element One Hydrogen & Critical Minerals Arranges Financings and Initiates Marketing Campaign https://bit.ly/4oGujeW

- June 23, 2026 – American Tungsten Reports 125 Feet of Tungsten-Silver Mineralization https://bit.ly/4acDLky

- June 23, 2026 – Power Metallic reports New Lion drill intercepts of 13.30 Meters of 3.98% CuEqRec¹ in Hole 26-115 and 5.26 Meters of 8.45% CuEqRec¹ in Hole 26-105 at Lion https://bit.ly/4ahSyu7

- June 23, 2026 – Spartan Metals’ Exploration Program Confirms Tungsten Skarn Discoveries at past Producing Mine at Eagle Project, Nevada https://bit.ly/4gARpSi

- June 22, 2026 – Ucore Produces NdPr Oxide and Ships Qualification Samples to Major Rare Earth Magnet Manufacturers https://bit.ly/4exoU5j

- June 22, 2026 – Greenland Mines Signs Drilling Contract with Nordisk Fundering for Expanded 2026 Skaergaard Diamond Drilling Program in Greenland https://bit.ly/4uSfuHR

- June 22, 2026 – Deep Sea Minerals Corp. Welcomes G7 Leaders’ Declaration on Securing Critical Minerals Supply Chains https://bit.ly/4vk2Pyk

- June 22, 2026 – Resolution Accepted Into Membership in the US Defense Industrial Base Consortium (Or “DIBC”) https://bit.ly/43Q4kIx

About the Critical Minerals Institute (CMI)

The Critical Minerals Institute (CMI) is a global think tank for the critical minerals economy, serving as a central hub that connects companies, capital markets, and policymakers, and delivering actionable intelligence through its monthly CMI Masterclasses, weekly Critical Minerals Report (CMR), twice-monthly CMR Podcasts, bespoke research, and board-level advisory services across exploration finance, supply chains, and geopolitics. CMI also organizes its flagship annual event, CMI Summit – The Brain Trust of the Critical Minerals Economy, a global gathering of government leaders, institutional investors, policymakers, and industry executives. CMI Summit 6 is scheduled for May 17–18, 2027, at Toronto’s Fairmont Royal York. For more information on the CMI, go to Critical Minerals Institute (CMI).