Jack-in-the-Stox: Neo Performance Materials and the Rare Earth Permanent Magnet Supply Chain

written by Jack Lifton | June 17, 2026

In this ongoing “Jack-in-the-Stox” Q&A series, Jack Lifton examines the companies, technologies, and geopolitical realities shaping the global critical minerals economy. Each week, Lifton offers direct commentary and analysis on the questions, claims, and strategic developments driving today’s rapidly evolving critical minerals sector.

Neo Performance Materials Inc. (TSX: NEO | OTCQX: NOPMF) is increasingly discussed in connection with the long-term demand for rare earth permanent magnets, which are central to electrification technologies such as electric vehicles and wind power. The broad investment logic is relatively intuitive: permanent magnets are required in systems that are scaling globally, while the rare earth supply chain remains constrained and strategically sensitive. What is less intuitive—and more important for investors—is that end-market tailwinds do not automatically translate into stable shareholder returns. In practice, the pathway from industry growth to company profitability depends on execution, customer qualification progress, the ability to scale into commercial volumes, and the resilience of margins under cyclical and competitive pressure.

Permanent magnets matter because they enable efficient electromechanical conversion in applications prioritized for efficiency, performance, and emissions reduction. As these applications expand, magnet-containing components increasingly move from being experimental to being platform-level decisions. That transition can, in favorable cases, create a degree of purchasing durability once a supplier is qualified and embedded. At the same time, the rare earth and magnet input environment is historically volatile. Pricing for relevant inputs can swing with changes in supply balances, utilization rates, and competitive capacity. The presence of structural demand therefore, does not eliminate the need for careful underwriting of margin behavior and market dynamics.

A core driver behind investor interest in this space is the strategic concentration risk in the rare earth supply chain. Key processing and refinement capabilities have historically been concentrated in a limited number of geographies. This concentration can create practical problems for buyers: supply reliability, continuity of specification, and exposure to policy or geopolitical shocks. As a result, diversification efforts increasingly focus not only on securing material availability but also on obtaining a qualified, reliable supply that meets industrial requirements. The investment question is whether a company is positioned in segments of the value chain where buyers are willing to pay for reliability and performance rather than simply chasing commodity prices.

Neo’s relevance should therefore be framed in terms of value capture rather than category association alone. The fact that magnets are part of the future electrification story is only the starting point. The more meaningful question is whether Neo can participate in the magnet value chain in a way that converts technical adoption into repeatable revenue and sustainable margins. In a best-case scenario, customer qualification leads to repeat purchasing, and operational scaling translates into consistent shipments rather than sporadic demand. Investors should also evaluate whether Neo’s economic model can absorb input-cost swings and competitive pricing pressures without impairing profitability. This is a sector where being “in the right theme” can still be insufficient if scale-up does not translate into profitable throughput or if competition compresses pricing faster than management can respond.

Policy tailwinds reinforce the end-market direction for magnet-containing technologies. Electrification strategies and industrial policy initiatives can influence procurement pipelines and long-term investment plans. Even so, timing uncertainty is common. Projects can slip, incentives can be revised, and trade or regulatory conditions can shift. For that reason, an institutional approach should focus on observable execution milestones and customer traction rather than assuming that policy intent will immediately translate into company results.

Key risks remain central to the evaluation. Pricing and margin volatility can persist, particularly when supply-demand balances shift quickly. Customer ramp-ups may fall short of initial expectations due to engineering changes, qualification steps, or production planning adjustments. Competitive capacity additions can pressure pricing power, and operational execution risks such as yield, quality consistency, and scale-up discipline can materially affect outcomes. Finally, the policy and geopolitical environment can impact both supply access and demand timing, which means that investors should underwrite the possibility of non-linear outcomes rather than relying on straight-line growth assumptions.

For investors reviewing Neo, the most important diligence is not to treat the thesis as a binary bet on rare earth demand, but to connect fundamentals directly to the magnet narrative. The focus should be on the magnet-relevant portion of the revenue mix, evidence that customer qualification is progressing meaningfully, and whether revenue and margin trends suggest durable demand capture rather than temporary market effects. Operational progress toward realized capacity, together with management’s clarity on how near-term performance supports medium-term scaling, is especially important. In technical adoption-driven markets, the transition from potential demand to qualified supply is often the decisive factor separating strong outcomes from disappointing ones.

In conclusion, Neo Performance Materials appears positioned to benefit from the long-term electrification-driven growth in permanent magnet demand, alongside an increasingly important need for supply-chain diversification away from concentrated processing capacity. The investment case is directionally credible, but it remains execution-dependent: Neo must scale effectively, maintain margins through volatility, and convert industry tailwinds into sustained customer traction. For investors, this is best understood as an execution-oriented supply-chain thesis rather than a simple rare earth commodity exposure.

Kevin Keough on Preparing to Drill the Trek South Copper-Gold Target in the Golden Triangle

written by InvestorNews | June 17, 2026

In a recent InvestorNews interview with Tracy Hughes, Kevin Keough, CEO and Director of Oreterra Metals Corp. (TSXV: OTMC), discussed the company’s upcoming maiden drill program at Trek South, a copper-gold porphyry target located in British Columbia’s Golden Triangle. The discussion also covered a recently announced royalty transaction involving Enduro Metals Corporation and updates on the company’s exploration projects in British Columbia, Nevada, and Ontario.

For Keough, the excitement surrounding Trek South stems from one simple fact: this is not a previously drilled prospect being revisited. It is an entirely new target.

“We’ve developed the Trek South prospect as a new-to-science target over the last several years,” Keough explained. “Nature has basically given us a huge target that looks very juicy as a potential porphyry copper-gold discovery in the making.”

The target itself emerged as glacial retreat exposed previously inaccessible geology. Extensive fieldwork, mapping, geochemical analysis, and surface observations have led Oreterra’s technical team to believe they are drilling directly into a large porphyry system.

Unlike many early-stage exploration projects where drilling seeks to determine whether mineralization exists at all, Keough believes the company already has evidence that mineralized porphyry is present at surface.

“We can see the porphyry in the bare rock. We know there are values of metal right on surface, so we’ll be drilling in the system from day one.”

The initial phase of the program will comprise approximately 4,600 metres of drilling. While that may seem modest compared to larger development-stage projects, Keough emphasized that discovery—not resource definition—is the objective.

“What we need is one or two drill holes that give us several hundred metres of porphyry-style grades. If we achieve that kind of thing, we’ll know very quickly what we have.”

Trek South’s location further strengthens the investment thesis. The property is situated immediately adjacent to the Galore Creek project, one of Canada’s largest undeveloped copper-gold-silver deposits. Galore Creek is currently held through a joint venture between Newmont Corporation and Teck Resources Limited.

“Our property essentially injects itself into a massive land package controlled by the majors,” Keough noted. “We’re about six kilometres from Galore Creek. If we succeed, we’re strategically positioned right next door.”

The Golden Triangle has long been recognized as one of the world’s premier mineral districts, hosting numerous major discoveries and producing mines. The combination of world-class geology, improving infrastructure, and growing strategic demand for copper has placed renewed attention on the region.

For Oreterra, the objective is clear.

The company is seeking the type of large-scale porphyry system that major mining companies ultimately acquire and develop.

“We find these beasts, advance them, quantify them, and potentially sell them,” said Keough. “That’s exactly what we did at GT Gold with the Saddle North discovery.”

Keough’s reference to GT Gold is particularly relevant. As former CEO of GT Gold Corp., he helped lead the discovery and advancement of the Saddle North copper-gold porphyry deposit, which ultimately attracted the attention of Newmont Corporation. The company was acquired in a transaction valued at approximately C$456 million.

That experience is directly influencing Oreterra’s approach to Trek South.

“We learned how to drill these systems, how to define them, and how to position them for acquisition,” Keough said. “We’re essentially replicating that successful model.”

Alongside its exploration efforts, Oreterra has also been advancing a potentially valuable royalty asset.

The company recently announced a transaction involving Enduro Metals and the Newmont Lake property. The agreement would provide Enduro with an option to reduce an existing royalty burden while generating significant value for Oreterra.

According to Keough, the transaction could ultimately exceed $22 million through a combination of cash, shares, and future royalty-related payments.

“It’s a good example of how valuable royalties in the Golden Triangle can become,” he said. “Even in the near term, we’re looking at meaningful cash and share payments.”

While the long-term value of the transaction will depend on exploration success at Newmont Lake, Keough noted that initial consideration could provide important non-dilutive funding for Oreterra’s ongoing programs.

The company’s broader project portfolio also continues to evolve.

In Nevada, Oreterra is advancing the Kinkaid property within the Walker Lane trend, where recent fieldwork has identified what management believes may be a large porphyry system. In northwestern Ontario, the Lundmark Lake project is attracting renewed attention due to its proximity to the Musselwhite gold district and the presence of multiple volcanogenic massive sulphide and intrusive-related targets.

Despite these opportunities, management remains focused on Trek South.

“This summer is about Trek South,” Keough emphasized. “If we hit, we’re going full on.”

The timing may prove advantageous.

Copper has emerged as one of the world’s most strategically important metals, driven by electrification, artificial intelligence infrastructure, energy transition investments, and growing concerns about future supply deficits. Gold, meanwhile, continues to benefit from geopolitical uncertainty and central bank demand.

Trek South also contains silver, tungsten, and tellurium mineralization, providing potential exposure to additional strategic commodities. However, Keough remains focused on the project’s primary targets.

“Most of the rock value, if we really hit it, will be in the copper and the gold.”

For investors who follow early-stage exploration, few events carry greater significance than a maiden drill program on an undrilled target. It represents the moment when years of geological interpretation are finally tested against reality.

As Oreterra prepares to mobilize drills into the Golden Triangle, the coming weeks could determine whether Trek South joins the growing list of significant discoveries emerging from one of Canada’s most productive mining districts.

And if Keough’s confidence proves well-founded, the company may soon find itself advancing another major copper-gold system in a region already attracting the attention of some of the world’s largest mining companies.

Watch the full InvestorNews interview with Kevin Keough, CEO & Director of Oreterra Metals Corp. (TSXV: OTMC), to learn more about the Trek South drill program, the Enduro royalty transaction, and the company’s broader exploration strategy.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

Why Gina Rinehart Just Bet US$1 Billion on SpaceX

written by Tracy Hughes | June 17, 2026

When Gina Rinehart writes a billion-dollar cheque, investors should pay attention—not because she is always right, but because she doesn’t do anything with her capital without a win-win strategy.

This week, the executive chairman of Hancock Prospecting, Australia’s largest private mining company, confirmed that her firm has acquired a stake in Space Exploration Technologies Corp. (NASDAQ: SPCX) (“SpaceX”) reportedly valued at more than US$1 billion, making it the largest investment outside Hancock’s core iron ore business in the company’s history. Rinehart described SpaceX as a company operating in sectors that are “crucial” and praised the leadership of Elon Musk, while also hinting at future collaboration involving artificial intelligence and critical minerals.

At first glance, the investment appears straightforward. SpaceX has become one of the world’s most remarkable corporate success stories. The company transformed launch economics through reusable rockets, built Starlink into a global communications network, secured strategic government and defense contracts, and recently completed what many are calling the largest initial public offering in history. Investors have rewarded that success with a valuation exceeding US$2 trillion.

Yet viewing Rinehart’s investment solely through the lens of aerospace misses something important.

The real story may be found not in the skies above us, but in the ground beneath our feet.

For decades, mining investors have understood a simple truth: industrial revolutions are ultimately constrained by materials. Railways required steel. Electrification required copper. The digital age required silicon. The energy transition requires lithium, rare earths, nickel, graphite, uranium, copper, and a growing list of critical minerals.

Space exploration will be no different.

Earlier today, Critical Minerals Institute (CMI) Co-Chair Jack Lifton advanced a provocative argument. If humanity intends to establish a permanent presence on the Moon—or eventually on Mars—the challenge is not merely one of transportation. It is one of metallurgy.

Civilizations, Lifton argues, are not built on rockets. They are built on structural steel.

The ability to repeatedly manufacture steel capable of surviving extreme temperature fluctuations, thermal cycling, and harsh extraterrestrial environments may ultimately prove more important than the ability to launch payloads into orbit. The critical question is not how to reach the Moon. The critical question is how to stay there.

Viewed through that lens, SpaceX begins to look less like a technology company and more like the cornerstone of a future industrial ecosystem.

Permanent lunar infrastructure would require iron, molybdenum, chromium, vanadium, rare earth elements, copper, aluminum, titanium, energy systems, processing facilities, communications networks, and advanced manufacturing. Every one of those requirements traces directly back to mining, refining, metallurgy, and supply chains.

This is where the Rinehart investment becomes particularly interesting.

Hancock Prospecting has spent the past several years quietly expanding beyond iron ore. The company has accumulated positions across rare earths, lithium, copper, defense-related industries, and critical minerals assets. It has also increased its exposure to sectors tied to national security and advanced manufacturing. The company has already suggested that future collaboration with SpaceX could involve supplying critical minerals essential to advanced technologies.

In other words, Rinehart may be seeing something that many investors have not yet fully appreciated.

If SpaceX succeeds in transforming humanity into a space-faring civilization, it will require extraordinary quantities of steel, copper, aluminum, titanium, rare earth elements, uranium, graphite, lithium, molybdenum, vanadium, tungsten, and dozens of other minerals that rarely feature in popular discussions about space. Rockets may capture public imagination, but industrial civilization has always been built from materials.

The company could one day become one of the largest consumers of critical minerals in history.

That possibility alone changes the investment discussion.

Traditionally, investors evaluate SpaceX by examining launch cadence, satellite revenues, government contracts, artificial intelligence initiatives, or the ambitions of Elon Musk. Those metrics remain important. Yet they may represent only the first chapter.

The second chapter could be space industrialization.

History suggests that exploration eventually gives way to construction. Exploration creates headlines. Construction creates economies. Consider the historical precedent. The California Gold Rush created prospectors. The transcontinental railway created an economy. The Apollo program planted a flag. A permanent lunar presence would require mines, refineries, power systems, communications networks, manufacturing facilities, transportation corridors, and housing. Exploration is an event. Industrialization is an economy.

The American frontier was not transformed by wagon trains. It was transformed by railways, steel mills, mines, ports, power systems, and factories. The same pattern may ultimately emerge beyond Earth.

If that occurs, the winners may not simply be aerospace companies. They may include the miners, processors, refiners, metallurgists, manufacturers, and infrastructure providers capable of supporting a permanent industrial presence beyond our planet.

That does not automatically make SpaceX a compelling investment today.

Valuation still matters.

A company valued at more than US$2 trillion already incorporates extraordinary expectations. Investors purchasing shares today are not buying a small entrepreneurial venture. They are buying one of the largest companies in modern history. Future success alone may not be enough; the company must exceed expectations that are already exceptionally ambitious.

There are also execution risks. SpaceX continues to pursue highly ambitious objectives, including Mars settlement, orbital infrastructure, advanced artificial intelligence integration, and next-generation launch systems. Such projects require substantial capital, long timelines, and tolerance for technological uncertainty.

Investors should also consider the governance implications of any enterprise that remains strongly associated with a single, high-profile founder. Regardless of operational success, concentrated leadership structures can introduce succession, reputational, and execution risks that may become increasingly relevant as organizations mature and expand.

Yet perhaps those are not the most interesting questions.

The more interesting question is why one of the world’s most successful mining investors would commit more than US$1 billion to a company best known for rockets.

The answer may be that Gina Rinehart is not investing in rockets.

She may be investing in the future demand for everything required to build an industrial civilization beyond Earth.

If Jack Lifton is correct, and if permanent settlement of the Moon ultimately depends upon metallurgy, steelmaking, and critical minerals supply chains, then SpaceX may represent something larger than a space company.

It may represent the first major customer of an entirely new industrial economy.

The question for investors, therefore, is not whether SpaceX can reach the Moon. The company has largely demonstrated that capability already.

The more consequential question is whether humanity can build an economy there.

If the next great economic frontier is not space exploration but space industrialization, then the value of critical minerals may extend far beyond the Earth’s surface.

That possibility may explain why Gina Rinehart’s billion-dollar investment looks less like speculation and more like strategic positioning.

Control of resources helped build the last industrial age.

Control of the systems that transform those resources into infrastructure may define the next one.

Which brings us back to Gina Rinehart.

Billion-dollar investors rarely tell the market what they are thinking. They simply position themselves accordingly.

If the future of space is not exploration but industrialization, then this week’s investment may prove to be less about rockets than about steel, critical minerals, and the supply chains required to build a civilization beyond Earth.

This week, one of the world’s most successful mining investors may have quietly placed a US$1 billion wager on exactly that proposition.

Control of resources built the last industrial age.

Control of the systems that transform those resources into infrastructure may define the next one—on Earth and beyond.

How to stay on the moon after we get there

written by Jack Lifton | June 17, 2026

Our civilization is built on structural steel. This is the most necessary metal in history. It is not an iridium asteroid that we need to find as in the popular television series “For All Mankind.” If we are to colonize the Moon and perhaps Mars, we will need structural steel that can withstand the wide temperature variations on those airless bodies.

Building Off-World Structural Steel: Fe-First Autonomy and the Mo→Cr→V Substitution Path

Space industrialization is not constrained by whether iron exists off-world—it is constrained by whether a civilization can repeatedly manufacture structural materials with predictable properties. For early lunar and solar-system expansion, this means producing steels that can maintain performance under two demanding regimes: cryogenic toughness and high-temperature stability, including thermal-cycling durability in the ~500–650°C range.

This article explains a pragmatic, investor-oriented roadmap for developing off-world structural steel using a de-risked sequence: Fe-first autonomy followed by a staged substitution of alloying inputs—initially Mo (Molybdenum), then Cr (Chromium), then V (Vanadium)—implemented via adaptive “packet families” produced primarily on the Moon.

Why “Fe-first” matters for reducing early risk

Early manufacturing is not the time to chase every alloying detail simultaneously. The first breakthrough is to establish an off-world supply chain that can reliably produce steelmaking feedstock from locally mined material. That is what “Fe-first” accomplishes.

In a Fe-first approach, the Moon becomes the grade-making center: lunar extraction and refining convert Fe-bearing regolith or concentrates into melt feedstock with controlled chemistry. During initial deployments, Earth provides a baseline of qualified alloy additions and metallurgical know-how to ensure that the first certified steel grades meet cryogenic toughness and 500–650°C cycling durability requirements.

Asteroids can be supportive—especially for Fe-rich feedstocks—but they are not relied upon early for alloy precision. Their value is primarily logistical and capacity-based (diversifying input supply and reducing launch dependence), while the Moon carries the burden of producing repeatable, certifiable outcomes.

The Moon as the “metallurgical certification factory.”

The properties you care about—cryogenic toughness and hot-cycling durability—are fundamentally driven by metallurgical quality, not merely by the existence of metals. In practice, success depends on:

melt chemistry control (especially major alloying targets),

heat-treatment repeatability,

microstructure and defect management, and

quality assurance and performance testing tied to certified specifications.

These are precisely the kinds of capabilities that favor a dedicated, stable industrial base. The Moon is best suited to host the furnace infrastructure, the process instrumentation, and the QA loops required to turn variable mined feedstock into standard rolled shapes (beams and plates) with predictable performance.

From baseline grades to alloy autonomy: Mo →Cr →V

Once Fe-based steelmaking is proven and rolled products are certified, the next step is alloy substitution. For 500–650°C thermal-cycling durability, the alloying story is less about extreme combustion chemistry and more about maintaining microstructural stability against thermal softening, crack initiation, and fatigue during repeated temperature excursions.

Conceptually, the prioritization follows a performance-informed progression:

Mo (Molybdenum) first—supporting strength retention and stability across cycling conditions.

Cr (Chromium) next—improving high-temperature durability and supporting stable structural behavior.

V (Vanadium) later—contributing to strengthening mechanisms and microstructure stability depending on the steel family.

However, the real engineering and investment insight is that the substitution strategy should not be treated as a one-variable-at-a-time scientific experiment. In a mining and refining reality, feedstock varies. A risk-minimizing system needs a way to translate variability into repeatable melt chemistries.

That is where the concept of adaptive spec packets becomes essential.

Adaptive “spec packet families”: standardization with built-in flexibility

Instead of creating a unique alloy recipe every time mined material changes, the Moon should produce a small number of packet families—each family corresponds to a narrow target window for the major Mo/Cr/V composition relevant to the certified steel grades.

Incoming lunar (or asteroid-sourced) materials are assayed and then assigned to the best-fitting packet family. The refining and blending system adjusts to hit the major alloying targets tightly while keeping impurities within an acceptable band.

This packet-family model provides three investor-critical advantages:

Operational simplicity: fewer moving parts than fully bespoke chemistry every batch.

Certification efficiency: performance testing and qualification can be structured around packet families and heat-treatment recipes.

Manufacturing traceability: each rolled output is tied to a known packet class, enabling auditors and customers to verify the link between input chemistry and performance.

It is a manufacturing approach analogous to software-controlled calibration: you don’t eliminate variability; you govern it.

Mostly Moon sourcing: why it reduces technical uncertainty

Your thesis prioritizes mostly lunar sourcing for the alloying ramp. That choice aligns directly with property predictability. Alloying substitutions are only investable when the factory can repeatedly hit composition windows and maintain stable metallurgical responses.

Earth remains the early anchor for certification because it reduces the probability of failure during the learning phase. Asteroids can support feedstock continuity (especially Fe), but the alloying ramp is best managed where the QA system, refining infrastructure, and blending control are already operational—again reinforcing the Moon’s role.

Conclusion: a practical investor roadmap for space steel

A credible off-world structural steel industry will not start by solving the hardest material science problem first. It will start by building the industrial capability to certify repeatable performance.

The most investable path is:

Fe-first autonomy to establish reliable steelmaking and standard rolled shapes,

then a staged Mo → Cr → V alloy substitution,

implemented through adaptive packet families that preserve tight control of major alloy chemistry while maintaining impurity bands within allowable limits.

With this framework, the Moon becomes the grade-making hub and investors gain a clear milestone pathway: from certified baseline rolled steel to recertified higher-autonomy grades—without requiring the entire space supply chain to be perfect on day one.

Jim Atkinson on New High-Grade Zones and the Expanding Exploration Potential at Antimony Resources’ Bald Hill Project

written by InvestorNews | June 17, 2026

During a recent InvestorTalk interview hosted by Tracy Hughes, Jim Atkinson, CEO and Director of Antimony Resources Corp. (CSE: ATMY | OTCQB: ATMYF), discussed the Company’s latest assay results, progress toward a maiden resource estimate, and the Bald Hill project potential in New Brunswick.

A significant focus of the discussion was the Company’s recently announced trench sampling results from several newly identified zones located outside the established Main Zone. According to Atkinson, one of those areas, known as the Marcus Zone, was not previously known before being discovered through Antimony Resources’ exploration efforts.

The new zones have attracted considerable attention because they contain surface expressions of stibnite, the primary antimony-bearing mineral. Unlike the Main Zone, which has already been extensively drilled, these newly identified targets have seen little historical exploration.

Atkinson explained that the discovery of multiple mineralized zones beyond the Company’s existing drill-defined area has strengthened management’s belief that additional exploration may identify a broader mineralized footprint at Bald Hill. While the overall dimensions of the mineralization remain unknown, ongoing drilling and trenching continue to expand the Company’s understanding of the project.

The Company’s next exploration program is expected to include approximately 18,000 metres of drilling, one of the largest programs undertaken on the property to date. The drilling will serve a dual purpose: advancing the project toward a resource estimate while simultaneously testing the broader exploration potential of the district.

A key milestone for Antimony Resources is the completion of a maiden mineral resource estimate. Atkinson noted that much of the groundwork required for that objective has already been completed.

The Company believes it has achieved the drill-hole spacing necessary to support resource modelling, having completed drilling at intervals significantly tighter than 50 metres. Independent consultants working with the Company have indicated that the spacing should provide sufficient confidence for geological modelling and resource estimation.

In addition to drilling density, Antimony Resources has implemented the quality assurance, quality control, and chain-of-custody procedures required to support future resource calculations. These measures include sample tracking protocols, secure storage facilities, and standardized operating procedures designed to help ensure the integrity of exploration data.

While advancing toward a resource remains an important objective, management appears equally focused on the exploration potential represented by the newly discovered zones.

Recent sampling from the South Zone returned 38 grab samples averaging 19.5% antimony, including one sample grading 44% antimony. The results confirmed the presence of high-grade stibnite mineralization at surface and provided further evidence that mineralization extends beyond the Main Zone.

Current drilling is focused on the Central Zone, located approximately 150 metres south of the Company’s southernmost drill hole in the Main Zone. Management believes the two zones may ultimately prove to be connected. If future drilling supports that interpretation, the mineralized trend could extend an additional 200 to 300 metres to the south, increasing the known strike length to nearly 1.5 kilometres.

Another target area located approximately 900 metres farther south remains largely unexplored and is expected to play an important role in determining the extent of mineralization across the property.

Atkinson also highlighted what he views as one of Antimony Resources’ most important competitive advantages. Unlike many projects promoted as antimony opportunities, Bald Hill is not primarily a gold deposit containing antimony as a secondary product.

Many of the world’s best-known antimony occurrences are associated with gold mineralization, where antimony grades are often relatively low and economic decisions are driven primarily by gold production. Bald Hill, by contrast, is being advanced specifically as an antimony project, giving investors direct exposure to antimony rather than to a by-product credit associated with another commodity.

As antimony has emerged as one of the world’s most strategically significant critical minerals, governments have begun paying closer attention to projects that could contribute to future domestic and allied supply chains.

That growing interest was reflected recently when New Brunswick’s Minister of Natural Resources, the Honourable John Herron, visited the Bald Hill project alongside senior officials from the provincial government. The delegation included the Assistant Deputy Minister, the Director of Resource Development, and Senior Geologist Kay Thorne, who originally identified the occurrence during regional mapping work in 2005.

According to Atkinson, the visit underscored both the province’s support for mining development and the increasing importance of antimony within Canada’s critical minerals strategy.

The Company has also continued investing in site infrastructure, including road improvements and water management systems designed to improve year-round operating conditions. Management reported that upgrades completed over the past year have significantly improved site access and reduced seasonal challenges experienced during previous exploration campaigns.

With drilling underway, new zones being tested, and preparations continuing for a maiden resource estimate, Antimony Resources appears to be entering a significant phase in the development of Bald Hill. Upcoming drilling and exploration results are expected to provide additional insight into both the size of the potential resource and the broader exploration potential of the property.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here.

Critical Minerals Report (06.14.2026): Control is the New Commodity

written by Tracy Hughes | June 17, 2026

“I didn’t think I would live long enough to see someone recommend that investors take a hard look at processing technology companies, but I guess that time has arrived.”— Jack Lifton, Co-Chair, Critical Minerals Institute (CMI)

The past week may ultimately be remembered as the moment when critical minerals ceased being discussed primarily as commodities and became openly recognized as instruments of industrial policy. Across Washington, Brussels, Tokyo, New Delhi, Kinshasa, Jakarta, and Brasília, governments and corporations continued to make decisions that increasingly resemble infrastructure planning rather than resource development. The common thread running through nearly every major development was not geology — it was control.

For several years, the industry has spoken about diversification away from China. During the past week, however, the discussion shifted noticeably from aspiration to urgency. A report from the U.S.-China Business Council stated that some critical minerals sourced from China remain “nearly unobtainable” despite ongoing trade discussions, with companies reporting continued difficulties securing materials essential to advanced manufacturing. Three-quarters of affected firms are now actively seeking alternative sources, underscoring how export controls have become a structural feature of the market rather than a temporary negotiating tactic.

The restrictions are already reshaping industrial planning throughout the developed world. Chinese export data released this week showed continued strength in advanced manufacturing exports, particularly semiconductors, integrated circuits, and data-processing equipment. While Western governments accelerate efforts to diversify upstream supply chains, China continues to capture significant value downstream through manufacturing and technology production. The result is a growing recognition that supply-chain resilience requires more than access to raw materials; it also requires industrial capacity.

The implications were immediately visible in the tungsten market.

Reports emerged that U.S. tungsten scrap exports to Japan have surged as buyers scramble to secure material following Chinese restrictions. At the same time, investigations revealed that Chinese buyers have been aggressively pursuing tungsten scrap throughout North America, creating what some industry participants describe as an increasingly intense competition for secondary supply. Tungsten is no longer simply a specialty metal. It has become a strategic material underpinning aerospace, defense, semiconductor manufacturing, and industrial tooling.

The significance of tungsten extends beyond the metal itself. The market offers a preview of what may happen across numerous critical mineral supply chains as governments prioritize domestic security over traditional notions of market efficiency. Scrap, recycling, stockpiles, and refining capacity are becoming as important as primary production.

Japan provided perhaps the clearest illustration of this shift.

One of the week’s most important developments was the announcement that Shin-Etsu Chemical Co., Ltd. (TSE: 4063) intends to establish a new rare earth refinery in Japan. The project represents another step in Tokyo’s long-running effort to reduce dependence on Chinese rare earth processing and follows a series of initiatives that include stockpiling, recycling programs, international partnerships, and deep-sea rare earth exploration.

The announcement arrives against the backdrop of continuing restrictions on heavy rare earth exports from China. Dysprosium, terbium, yttrium, and other heavy rare earth elements remain among the most difficult materials for non-Chinese manufacturers to secure. Japanese companies have already reported disruptions to portions of the magnet supply chain, highlighting how dependent advanced economies remain on Chinese processing capacity despite years of diversification efforts.

This context also helps explain why reports surfaced this week that the United States has asked China to resume certain rare earth exports to Japan. While the request may appear diplomatic in nature, it underscores a deeper reality. The industrial economies of North America, Europe, and Asia remain interconnected. Supply disruptions affecting Japanese manufacturers quickly ripple through automotive, electronics, aerospace, and defense supply chains across allied nations.

Meanwhile, Washington continued to move beyond rhetoric and toward legislative action.

Congressman John Moolenaar (R-Michigan), Chairman of the U.S. House Select Committee on Strategic Competition between the United States and the Chinese Communist Party, and Congressman Ro Khanna (D-California), the Committee’s Ranking Member, introduced the Magnets Value Chain Support Act of 2026, bipartisan legislation designed to encourage domestic magnet manufacturing through targeted tax incentives. The proposal seeks to support the entire value chain, from rare earth oxide production through magnet manufacturing and ultimately into defense systems, electric motors, and advanced industrial applications.

The legislation is significant because it acknowledges a reality that many policymakers previously avoided. The United States does not merely need more rare earth mines. It needs more industrial capacity. Mines without separation facilities, metallization capabilities, alloy production, magnet manufacturing, and downstream customers do not create resilient supply chains. They create inventories.

This distinction was explored in Jack Lifton’s InvestorNews column, “Floor Pricing Won’t Rebuild America’s Rare Earth Industry — It Will Break It,” which argued that policy discussions focused exclusively on supporting mining projects risk overlooking the more difficult challenge of rebuilding entire industrial ecosystems. The rare earth industry has repeatedly demonstrated that capital alone cannot create supply chains. Expertise, infrastructure, customers, and technical capacity must also exist.

That challenge is becoming increasingly visible outside North America as well.

Brazil continues to emerge as one of the most strategically important jurisdictions in the global effort to diversify rare earth supply chains. Reporting this week highlighted growing international interest in Brazilian rare earth projects and reinforced the country’s position as a potential cornerstone of future Western supply chains. Unlike many jurisdictions, Brazil combines substantial geological potential with an increasingly sophisticated mining sector and expanding downstream ambitions.

The European Union is pursuing a different approach. Brussels is reportedly considering rules designed to reduce reliance on China through broader supply-chain diversification requirements. Rather than attempting to replicate every stage of the supply chain domestically, Europe appears increasingly focused on ensuring that no single country can dominate critical inputs across strategic sectors. Such policies would represent another step toward embedding supply-chain resilience directly into industrial regulation.

The broader pattern is becoming difficult to ignore.

Japan is investing in refining. Europe is developing diversification requirements. The United States is promoting magnet manufacturing. India is advancing integrated processing strategies. Brazil is positioning itself as an alternative source of supply. Different governments are pursuing different paths, but the destination is remarkably similar.

Control of critical mineral supply chains is increasingly being treated as a matter of national competitiveness.

The battery materials sector provided another example of how quickly geopolitical decisions can reshape markets.

The Democratic Republic of Congo’s restrictions on cobalt exports continue to reverberate throughout global supply chains. Reports this week indicated that shortages of cobalt hydroxide feedstock are tightening conditions for refiners and battery manufacturers. What began as a domestic policy decision has evolved into a global supply constraint affecting one of the most important battery materials markets. The development reinforces an increasingly important lesson for investors: concentration risk exists not only in processing but also in production.

At the same time, General Motors Company (NYSE: GM) made headlines by backing sodium-ion battery technology through a partnership aimed at stationary energy storage markets. The announcement should not be interpreted as a threat to lithium-ion batteries. Rather, it reflects the growing segmentation of energy storage technologies.

The battery economy is becoming increasingly diversified. Different chemistries are being optimized for different applications. Lithium remains dominant in transportation. Sodium-ion is finding opportunities in grid-scale storage. Other chemistries continue to emerge for specialized applications. For investors, this suggests that future demand growth may be distributed across a broader range of critical minerals than previously anticipated.

Nickel remains the notable exception.

Despite its strategic importance, the nickel market continues to struggle with oversupply. Indonesia’s rapid expansion has fundamentally altered market dynamics, and new Indonesian mining regulations announced this week (Forbes) have raised questions about the future direction of investment in the sector. Some analysts believe the regulatory changes could encourage portions of the Chinese-backed nickel industry to seek opportunities elsewhere, potentially accelerating investment into alternative jurisdictions.

Yet nickel’s experience also serves as a cautionary tale.

Strategic importance does not guarantee scarcity pricing.

Few minerals are more essential to modern industry than nickel. Yet years of aggressive capacity expansion have created persistent oversupply and weak prices. The lesson extends well beyond nickel. Investors evaluating critical minerals projects must distinguish between strategic relevance and economic scarcity. The two are not always the same.

Another material quietly moved into the spotlight this week: indium.

One of the most consequential stories of the past several days received surprisingly little mainstream attention. China’s control over indium phosphide exports is reportedly threatening portions of the rapidly expanding artificial intelligence infrastructure buildout. Indium phosphide plays a critical role in photonic semiconductors used in high-speed data transmission, making it increasingly important for AI data centers and advanced communications systems. Reuters reported that prices for certain indium phosphide wafers have surged dramatically as supply concerns intensify (Reuters).

The development is notable for two reasons.

First, it highlights why the Critical Minerals Institute recently added indium to the 2026 CMI Critical Minerals Watchlist. Second, it demonstrates how quickly obscure specialty materials can become strategically significant when technology evolves.

Few investors paid attention to indium five years ago.

Today, it sits near the center of one of the fastest-growing segments of the global economy.

Closer to home, Canada’s role in this evolving landscape remains increasingly important.

Our recent InvestorNews column, “Canada’s Critical Minerals Moment in a Fragmenting World,” examined the country’s unique position within North American supply chains. Canada possesses meaningful exposure to most of the minerals appearing on the CMI Watchlist, yet like many allied nations, continues to rely heavily on foreign processing infrastructure. The opportunity for Canada is therefore not merely geological. It is industrial.

This week’s discussion surrounding Canada’s estimated US$4.7 trillion infrastructure opportunity reinforces the same conclusion. Infrastructure, energy systems, transportation networks, ports, processing facilities, and industrial corridors will ultimately determine whether resource wealth translates into long-term strategic advantage.

Among the corporate developments highlighted through InvestorNews this week, several reflected the growing emphasis on critical minerals diversification. American Tungsten Corp. (CSE: TUNG | OTCQB: TUNGF) reported strong drilling results from its IMA Mine Project. Volta Metals Ltd. (CSE: VLTA) reported significant rare earth and gallium mineralization at its Springer Project and separately received support through Ontario’s Critical Minerals Innovation Fund. Scandium Canada Ltd. launched a new drilling campaign at Crater Lake, while Power Metallic Mines Inc. (TSXV: PNPN) completed a C$28.2 million financing that included participation from Eric Sprott.

Taken individually, these announcements are routine exploration and development news. Collectively, however, they illustrate something larger. Capital continues to flow toward projects positioned within supply chains viewed as strategically important by governments and industry.

That may be the defining lesson from the past week.

The critical minerals sector is no longer being shaped primarily by geology, commodity cycles, or even traditional mining economics. It is increasingly being shaped by policy frameworks, industrial strategies, trade relationships, processing capabilities, and national security considerations.

Rare earths, tungsten, cobalt, nickel, lithium, indium, gallium, scandium, and dozens of other materials are becoming components of a much larger conversation about economic resilience.

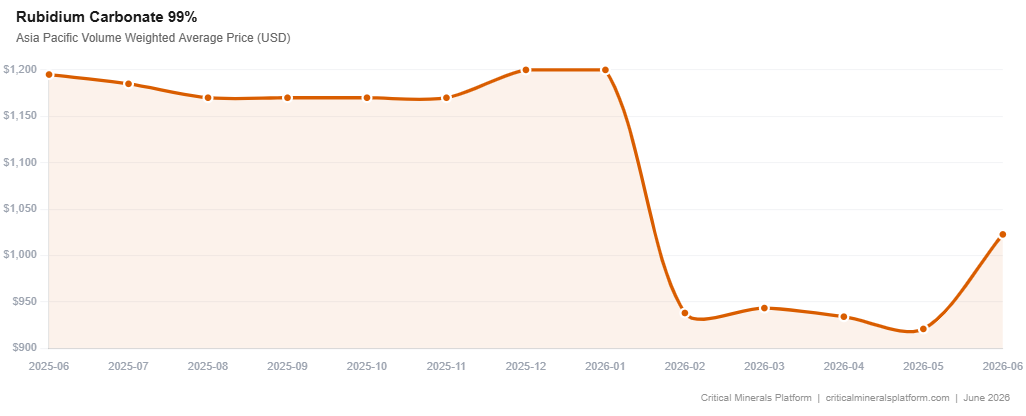

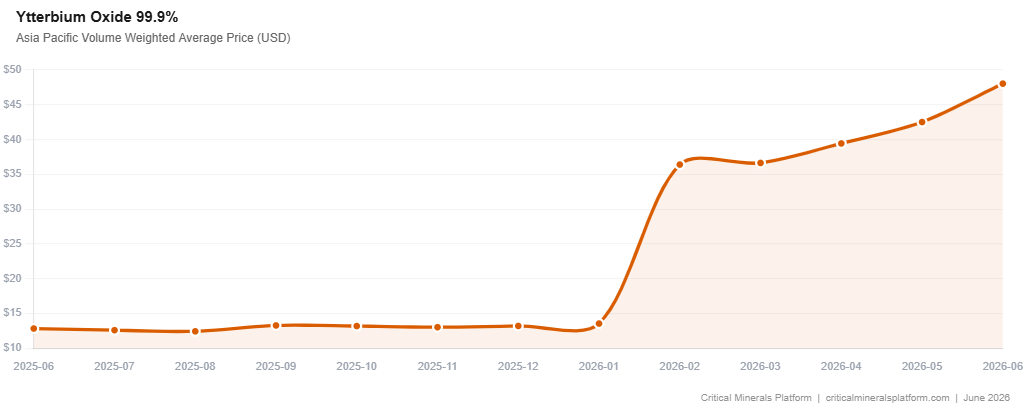

The week’s pricing activity also offered a reminder that strategic importance increasingly extends beyond the headline “criticals”. According to pricing data compiled by Critical Minerals Platform (CMP), rubidium carbonate (99%) rose 11.07% month-over-month to US$1,022.67 per kilogram, while ytterbium oxide (99.9%) increased 12.98% to US$48.02 per kilogram. Much like indium, these are materials that rarely dominate headlines until supply constraints or new technologies suddenly make them impossible to ignore.

For investors, the question is evolving.

The issue is no longer simply whether a mineral is critical.

The issue is whether a company, project, or jurisdiction occupies a position within a supply chain that the world can depend upon when access becomes uncertain.

That distinction is likely to define the next phase of the critical minerals economy.

Enjoy the Critical Minerals Report (CMR)?

Join the Critical Minerals Institute (CMI) and receive the CMR directly in your inbox each week.

For premium pricing data, market intelligence, and critical minerals insights, visit CriticalMineralsPlatform.com.

Get your first month free and save 20% with promo code CMI2026.

InvestorNews Critical Minerals Institute (CMI) Directorial Headline Picks for the Past Week:

June 10, 2026 – US tungsten scrap exports to Japan soar on Chinese curbs (Source)

June 10, 2026 – Shin-Etsu to set up rare-earth smelter in Japan to ease reliance on China (Source)

June 10, 2026 – Mobilizing Canada’s US$4.7T infrastructure opportunity (Source)

June 10, 2026 – US business group says some critical minerals are ‘nearly unobtainable’ from China (Source)

June 10, 2026 – DR Congo’s curbs on cobalt spark squeeze in vital battery element (Source)

June 09, 2026 – GM bets on sodium battery tech to challenge China dominance (Source)

June 09, 2026 – Moolenaar, Khanna Introduce Bipartisan Legislation to Reshore America’s Magnet Supply Chain (Source)

June 09, 2026 – Indonesia’s New Nickel Mining Rules Could Spark A Chinese Exodus (Source)

June 09, 2026 – US asks China to resume rare-earth exports to Japan (Source)

June 09, 2026 – China’s Strength in Semiconductors, Rare Earths Drives Export Surge (Source)

June 08, 2026 – The Fight to Break China’s Rare-Earth Dominance Moves to a New Front in Brazil (Source)

June 05, 2026 – EU weighs rules to cut reliance on China through broader supply chains (Source)

InvestorNews.com Media Updates:

June 12, 2026 – Sorting It Out: Critical Minerals or Crucial Materials? https://bit.ly/4elX8IU

June 10, 2026 – Jack-in-the-Stox: The Strategic Value Hidden Inside Appia’s Critical Minerals Portfolio https://bit.ly/3QtvLEW

June 10, 2026 – Floor Pricing Won’t Rebuild America’s Rare Earth Industry — It Will Break It https://bit.ly/43YF7vo

June 09, 2026 – Canada’s Critical Minerals Moment in a Fragmenting World https://bit.ly/4xjyGAF

June 08, 2026 – Detroit’s Lesson for Critical Minerals Investors: Supply Chains Cannot Be Financialized Forever https://bit.ly/3SqXWow

InvestorNews.com News Release Updates:

June 11, 2026 – West High Yield (W.H.Y.) Resources Ltd. Announces First Tranche Closing of Private Placement and Record Ridge Project Update https://bit.ly/4uroVh7

June 11, 2026 – West High Yield (W.H.Y.) Resources Ltd. Announces Court Dismisses Judicial Review Challenging Record Ridge Project https://bit.ly/4aFMMCA

June 11, 2026 – Renforth Resources Receives Initial Assay Results From 2026 Parbec Stripping Program; Standout Sample Returns 0.567 G/T Gold With Coarse Gold and Tungsten Signature https://bit.ly/4fz4fjz

June 11, 2026 – Scandium Canada Launches 4,000-Metre Diamond Drilling Program at Crater Lake https://bit.ly/4e4Vo8g

June 11, 2026 – Volta Metals Awarded Up to $500,000 from Ontario’s Critical Minerals Innovation Fund https://bit.ly/4vH7FW3

June 11, 2026 – Spartan Metals Corp Retains Strategic Government Relations Firm to Advance Non-Dilutive Funding Opportunities https://bit.ly/4gdRn2s

June 10, 2026 – Power Metallic Mines Announces Closing of Brokered LIFE Offering for Gross Proceeds of C$28.2 Million and Welcomes Eric Sprott as a New Shareholder https://bit.ly/4gb5upd

June 10, 2026 – Greenland Mines Executes Strategic Downstream Agreement on Helguvik Industrial Complex in Iceland https://bit.ly/4vDt7LN

June 10, 2026 – Voyageur Pharmaceuticals Ltd. Submits Multi-Year Area-Based Exploration Permit Application for Bulk Sampling and Feasibility Support at Frances Creek Barite Project https://bit.ly/4uvGBYR

June 10, 2026 – Resouro Executes Binding MOU for Novo Mundo Work Program https://bit.ly/4xCnXld

June 9, 2026 – Fox Tungsten Announces Symbol Change to “FOXTF” on the OTC Pink Market https://bit.ly/4xrbGjp

June 9, 2026 – Nord Precious Metals Mining Inc. to Present at the Emerging Growth Conference on June 10, 2026 https://bit.ly/4utjnTp

June 9, 2026 – Grid Metals Corp. Provides Update on Makwa Nickel-Copper-PGE Project https://bit.ly/4fw9fpb

June 9, 2026 – American Tungsten Reports Strong Drilling Results from Lower D-level https://bit.ly/4ogqHAn

June 9, 2026 – Spartan Metals Corp Engages The Howard Group to Direct Capital Market & Corporate Digital Communications Programs https://bit.ly/4uVjDeP

June 8, 2026 – Deep Sea Minerals Corp. Provides Strategic Execution Update https://bit.ly/4v3oJ98

June 8, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Results up to 44.2% Antimony from Trenching of the South Zone at Bald Hill https://bit.ly/43iOFRV

June 8, 2026 – Homerun Resources Inc. Completes CAPEX Budget for the 3N Primary Silica Sand Purification Plant https://bit.ly/4xvacoi

June 8, 2026 – Volta Intersects 0.81% Total Rare Earth Oxide and 68.13 g/t Gallium Oxide over 688m at Springer REE Project in Ontario, Canada https://bit.ly/49HQlYO

About the Critical Minerals Institute (CMI) The Critical Minerals Institute (CMI) is a global brain trust for the critical minerals’ economy, serving as a hub that connects companies, capital markets, and policymakers. Through CMI Masterclasses, the weekly Critical Minerals Report (CMR), bespoke research, and board-level advisory services, CMI delivers actionable intelligence spanning exploration finance, supply chains, and geopolitics. For more information on the CMI, go to Critical Minerals Institute (CMI).

Sorting It Out: Critical Minerals or Crucial Materials?

written by Tracy Hughes | June 17, 2026

“You like potato and I like po-tah-to, you like tomato and I like to-mah-to…” wrote lyricist Ira Gershwin in Let’s Call the Whole Thing Off (1937), with music by George Gershwin.

For nearly two decades, our industry has been having its own version of that debate.

In the early days, around 2008 and 2009, these materials were commonly referred to as “strategic materials” or “strategic minerals.” As the sector evolved, new labels emerged, including “battery metals,” “battery materials,” and “magnet metals.” We even tried to popularize the term “technology metals,” a phrase championed by Critical Minerals Institute (CMI) Co-Chair Jack Lifton long before critical minerals became a mainstream policy discussion. Earlier this week, CMI Co-Chair Melissa “Mel” Sanderson suggested another alternative: “crucial materials”.

Eventually, governments, industry associations, and investors settled on “critical minerals.” Today, the term is so widely accepted that few stop to ask a rather obvious question:

Are these materials actually minerals?

In many cases, the answer is no.

The reality is that many of the materials appearing on national critical minerals lists are not minerals at all. Copper is a metal. Uranium is a metal. Gallium is a metal. Rare earth elements are metals. Steel is an alloy. Antimony, germanium, and silicon are classified as metalloids.

The numbers tell an interesting story. Of the 24 materials on the CMI Watchlist, 20 are metals, 3 are metalloids, one is an alloy, and only one is clearly a mineral. Yet we continue to refer to the entire group as “critical minerals.”

Before we go any further, it is worth understanding the difference.

What is a Mineral?

A mineral is a naturally occurring inorganic substance with a defined chemical composition and crystalline structure. Graphite, quartz, and feldspar are all minerals.

Importantly, a mineral is not the same thing as a metal. Metals are often extracted from minerals through mining and processing. Copper is produced from copper-bearing minerals such as chalcopyrite. Aluminum is produced from bauxite. Lithium is recovered from minerals such as spodumene or from brines.

What is a Metal?

A metal is a chemical element that typically conducts heat and electricity and can be shaped without breaking. Copper (Cu), nickel (Ni), lithium (Li), uranium (U), tungsten (W), titanium (Ti), and aluminum (Al) are all metals.

Most of the materials appearing on government critical minerals lists are, in fact, metals rather than minerals.

What is a Metalloid?

A metalloid is an element that exhibits properties of both metals and non-metals. Silicon (Si), germanium (Ge), and antimony (Sb)—all included on the CMI Watchlist—are metalloids.

Their unique electrical properties make them indispensable to semiconductors, communications technologies, advanced manufacturing, and defense applications.

What Is an Alloy?

An alloy is a material composed of two or more elements, usually metals, designed to enhance performance characteristics such as strength, durability, or corrosion resistance.

Steel, which appears on the CMI Watchlist, is not a mineral and not a single metallic element. It is an alloy primarily composed of iron (Fe) and carbon (C), often with additional elements added to achieve specific industrial properties.

The 2026 CMI Watchlist by Scientific Classification

[*Light Rare Earth Elements (LREEs) | **Heavy Rare Earth Elements (HREEs) | ***Pm is the only REE with no stable isotopes; it occurs only in trace amounts naturally and is primarily reactor-produced.]

Viewed strictly through a scientific lens, only a small portion of what governments, investors, and industry participants call “critical minerals” are actually minerals. Most are metals. Some are metalloids. One is an alloy.

Yet the term “critical minerals” has won the branding war.

Does it matter?

Not particularly.

The more important question is not what we call these materials, but why we call them critical in the first place.

At the Critical Minerals Institute, we define criticality differently from many governments and organizations. Geological abundance is not the determining factor. Neither is market size.

A material becomes critical when the world depends upon a supply chain concentrated in one or two geopolitical jurisdictions where reliability risks exist.

As CMI Watchlist Editor Alastair Neill recently observed:

“A material becomes critical when its production is dominated by one or two countries—particularly where those jurisdictions present reliability risks to ongoing global supply.”

This distinction is important because criticality is not a geological concept.

It is a geopolitical and industrial concept.

Copper provides a useful example.

Copper is not scarce. Large copper deposits exist around the world. Yet copper has become increasingly critical because modern society cannot function without it. Electrification, artificial intelligence data centers, electric vehicles, transmission infrastructure, military systems, and renewable energy technologies all require enormous quantities of copper.

As demand rises faster than new mines can be developed, supply becomes strategically important.

Gallium offers another example.

Gallium is not particularly rare. It is produced as a byproduct of aluminum refining. The challenge is that China dominates production and processing. The risk is not the existence of gallium resources. The risk is concentration of supply.

The same pattern appears repeatedly throughout the critical minerals economy.

Rare earth elements are relatively abundant in the Earth’s crust. The issue is processing dominance.

Tungsten is not exceptionally rare. The issue is production concentration.

Indium and rhenium are not geologically unique. The issue is that they are produced primarily as byproducts, making supply difficult to increase when demand rises.

Even uranium, one of the world’s most important energy materials, owes much of its criticality to geopolitical considerations surrounding mining, conversion, enrichment, and fuel security.

This is why supply chains—not resources—define criticality.

The 2026 CMI Watchlist reflects this reality. Its Top 5 materials—Copper, Gallium, Tungsten, Uranium, and Rare Earth Elements—were not selected because they are the rarest materials on Earth. They were selected because they are foundational to modern economies, difficult to substitute, and exposed to geopolitical or processing risks that could disrupt supply.

Ultimately, the debate over whether these materials should be called minerals, metals, strategic materials, or critical materials misses the larger point.

The world does not have a critical minerals problem.

It has a critical supply chain problem.

And as governments, corporations, and investors increasingly discover, control of supply chains—not ownership of resources—will determine who succeeds in the next phase of the global economy.

Call them minerals.

Call them metals.

Call them crucial materials.

What matters is not what they are called.

What matters is who controls them.

Jack-in-the-Stox: The Strategic Value Hidden Inside Appia’s Critical Minerals Portfolio

written by Jack Lifton | June 17, 2026

In this ongoing “Jack-in-the-Stox” Q&A series, Jack Lifton examines the companies, technologies, and geopolitical realities shaping the global critical minerals economy. Each week, Lifton offers direct commentary and analysis on the questions, claims, and strategic developments driving today’s rapidly evolving critical minerals sector.

Investors in the critical minerals sector often make the mistake of valuing junior mining companies as if they were single-asset exploration stories. In reality, the companies most likely to create long-term shareholder value are those that assemble strategic positions in multiple supply chains before those supply chains become recognized as essential.

The market continues to view Appia primarily through the lens of exploration results. That view misses the larger picture. Appia has assembled positions in two of the most strategically important mineral sectors of the twenty-first century: rare earths and uranium.

Both are indispensable. Neither can be substituted.

Rare earth permanent magnets are the foundation of modern electrification, advanced manufacturing, robotics, and military systems. Uranium remains the only scalable, carbon-free baseload energy source capable of supporting the massive growth in electrical demand now being driven by artificial intelligence, data centers, electrification, and industrial reshoring.

The question for investors is not whether these materials will be needed.

The question is where secure supplies will come from.

Appia’s answer begins in Canada.

Its Alces Lake project in Saskatchewan remains one of the most significant rare earth discoveries in North America. What distinguishes Alces Lake is not merely its grades, although they have attracted considerable attention. More important are the presence of rare earth elements in the magnet—particularly neodymium, praseodymium, dysprosium, and terbium—that determine the strategic value of any rare earth deposit.

Western governments continue to search for secure non-Chinese sources of these materials. Alces Lake represents one of the few North American assets with the potential to become part of that supply chain.

At the same time, Appia maintains exposure to uranium through its Athabasca Basin properties. The Athabasca Basin is widely recognized as the premier uranium district in the world. As nuclear power returns to favor across North America, Europe, and Asia, strategic uranium resources in politically stable jurisdictions are becoming increasingly valuable.

But the most overlooked component of Appia’s valuation may be in Brazil.

The company’s relationship with Ultra Rare Earth Inc. gives Appia something unusual among junior mining companies: a meaningful equity interest in a separate vehicle advancing rare earth assets with district-scale potential.

Appia currently owns 25% of Ultra Rare Earth Inc., the company developing the PCH rare earth project and associated rare earth properties in Goiás State, Brazil.

This ownership position should not be viewed merely as a financial investment. It is effectively a strategic participation in a second rare earth development platform.

The PCH deposit is particularly noteworthy because it belongs to a class of rare earth deposits that has attracted increasing attention from both industry and governments. Ionic adsorption clay deposits have historically supplied many of the world’s heavy rare earth elements, and the search for comparable deposits outside China has become a priority for Western supply-chain planners.

By retaining a significant equity position in Ultra, Appia preserves exposure to PCH’s future value while sharing development risk and capital requirements with its partner.

In practical terms, Appia shareholders now possess indirect exposure to three distinct strategic asset groups:

Alces Lake and its magnet rare earth potential in Saskatchewan.

Athabasca Basin uranium properties in one of the world’s premier uranium jurisdictions.

A 25% ownership stake in Ultra Rare Earth Inc., which is advancing the PCH project and related Brazilian rare earth opportunities.

The market often struggles to value this type of portfolio because each asset belongs to a different stage of development and serves a different strategic supply chain.

Yet governments, defense planners, and industrial consumers increasingly understand the value of diversification across critical minerals.

Rare earths are becoming strategic.

Uranium is becoming strategic.

Jurisdictional security is becoming strategic.

Appia possesses exposure to all three themes.

The result is a company whose intrinsic value may ultimately prove substantially greater than that inferred from a conventional exploration-company valuation model.

Investors willing to look beyond quarterly drill results may conclude that Appia is not simply an exploration company. It is a strategically positioned critical minerals holding company with assets in two sectors that are becoming increasingly important to national security, industrial competitiveness, and the future of energy.

Floor Pricing Won’t Rebuild America’s Rare Earth Industry — It Will Break It

written by Jack Lifton | June 17, 2026

The United States is once again searching for a shortcut to rebuild its rare earth supply chain. This time, the idea gaining traction in Washington is government‑guaranteed floor pricing for rare earth oxides — a policy intended to stabilize domestic mining, counter Chinese price suppression, and encourage upstream investment.

It is an idea that sounds bold, decisive, and patriotic. It is also profoundly misguided.

Floor pricing does not solve the problem it claims to address. It misdiagnoses the strategic challenge, misallocates capital, entrenches subsidy dependence, and leaves the United States just as vulnerable to Chinese industrial strategy as before — perhaps more so.

If the U.S. wants a resilient rare earth supply chain, it must confront the real bottleneck: the absence of midstream and downstream processing capacity. Floor pricing does nothing to fix this. In fact, it actively diverts capital and political attention away from the parts of the supply chain that matter most.

This article explains why.

The Real Problem Isn’t Mining — It’s Processing

The United States does not lack rare earth ore. It lacks the ability to turn that ore into metals, alloys, and magnets — the components that power electric vehicles, wind turbines, precision‑guided munitions, and advanced electronics.

China’s dominance is not geological. It is industrial.

China controls:

80–90% of global separation capacity

Nearly all metallization and alloying capacity

Over 90% of NdFeB magnet production

Integrated industrial clusters that reduce cost and accelerate innovation

This is where strategic leverage comes from. This is where the value is created. And this is where the U.S. is weakest.

Floor pricing does not touch any of these segments.

Floor Pricing Misdiagnoses the Challenge

Floor pricing assumes the problem is low upstream prices. But upstream prices are low because China dominates the midstream and downstream. China can afford to depress oxide prices because it captures the value later in the chain.

Subsidizing U.S. mining does not change this dynamic.

It simply produces more concentrate that must still be shipped abroad for processing — often to China itself.

This is not a supply chain. It is a conveyor belt.

Floor Pricing Distorts Investment Incentives

Guaranteed prices attract capital — but not the kind of capital the U.S. needs.

Floor pricing incentivizes:

Marginal deposits

Fast‑to‑market juniors

Speculative upstream plays

Financial engineering over industrial capability

It does not incentivize:

Separation plants

Metallization

Alloying

Magnet factories

OEM qualification pipelines

These are the segments that determine whether the U.S. has a real rare earth industry or just a mine.

Floor pricing pushes capital toward the wrong end of the chain.

Price supports rarely sunset. Once established, they become politically impossible to remove.

Agriculture, biofuels, solar panels, steel — the pattern is always the same:

Subsidy introduced

Industry reorganizes around subsidy

Lobbying intensifies

Subsidy becomes permanent

Rare earths would be no different.

Floor pricing would create an industry dependent on government guarantees rather than competitiveness. And because rare earth prices are volatile, the political pressure to raise the floor would grow every time China pushes prices down.

Which brings us to the next problem.

China Can Undercut Any U.S. Floor Price Instantly

China has repeatedly demonstrated its willingness to use rare earth pricing as a geopolitical tool. If the U.S. sets a floor price, China can simply:

Flood the market

Depress global prices

Undercut the U.S. floor

Force Washington to raise subsidies

Repeat as needed

The U.S. cannot win a price war against a state‑directed industrial system that controls nearly all global processing capacity.

Floor pricing invites a contest the U.S. is structurally incapable of winning.

We Already Tried Upstream‑Only Support — It Failed

The MP Materials Corp. (NYSE: MP) experience is instructive.

The U.S. supported upstream production at Mountain Pass. The result:

Ore mined in the U.S.

Concentrate shipped to China

Value captured abroad

No domestic magnet industry created

Floor pricing would replicate this failure on a larger scale.

Where the Value Actually Is

Mining captures 3–5% of the value. Magnets capture 40–50%.

Floor pricing subsidizes the lowest‑value segment of the chain while ignoring the highest‑value segment.

This is not industrial strategy. It is industrial theater.

What the U.S. Should Do Instead

A serious rare earth strategy would focus on:

Guaranteed Offtake for Magnets and Metals – Not oxides. Finished components.

Defense Production Act Contracts – Tied to performance milestones, not price floors.

Accelerated Permitting for Midstream Facilities – Separation and metallization must be fast‑tracked.

Tax Credits for Magnet Production – Modeled on the 45X battery credit.

Allied Integration – Japan, Korea, Australia, and the EU must be part of the solution.

Recycling and Scrap Recovery – A domestic secondary supply is essential.

These tools build capability. Floor pricing does not.

Conclusion: Floor Pricing Is a Strategic Mistake

Floor pricing is politically attractive but strategically ineffective. It misdiagnoses the problem, misallocates capital, entrenches subsidy dependence, and fails to build the capabilities the U.S. actually lacks.

A resilient rare earth supply chain cannot be built on artificial prices. It must be built on processing, integration, and competitive industrial capacity.

Floor pricing is not a foundation. It is a crutch.

And the U.S. cannot afford to build its future in critical minerals on a crutch.

InvestorTalk Alert: Jim Atkinson from Antimony Resources Corp. to host on Thursday, June 11, 2026, at 9:00 AM EST

written by InvestorNews | June 17, 2026

InvestorNews.com is pleased to announce an upcoming InvestorTalk scheduled for tomorrow, Thursday, June 11, 2026, at 9:00 AM EST, featuring Jim Atkinson, CEO and Director, Antimony Resources Corp. (CSE: ATMY | OTCQB: ATMYF). To participate in this engaging discussion, please click here

Antimony Resources is an exploration and development company focused exclusively on Antimony. The Company’s management team possesses extensive experience in financing, exploration, development and mining. The Company is focused on becoming a significant North American producer of antimony.

In preparation for tomorrow’s InvestorTalk, here are some recent news releases from Antimony Resources for your review, which are listed below:

June 08, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Results up to 44.2% Antimony from Trenching of the South Zone at Bald Hill – click here

June 04, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) New Brunswick Minister of Natural Resources Visits Bald Hill Antimony Project – click here

May 13, 2026 – Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Results at the Bald Hill Antimony Deposit Including Intersections of 26.9% Antimony (Sb) – click here

We found the June 8th news release titled, “Antimony Resources Corp. (ATMY) (ATMYF) (K8J0) Announces Assay Results up to 44.2% Antimony from Trenching of the South Zone at Bald Hill” particularly noteworthy and here are 5 key data points from it:

High-Grade South Zone Assays – Rock samples from trenching at the South Zone returned very strong antimony values, with 38 samples averaging 19.5% Sb and individual assays reaching up to 44.2% Sb.

New Mineralized Zone Confirmed – The South Zone is located about 900 metres south of the Main Zone and appears to represent a separate, parallel but offset antimony trend, highlighting new exploration upside beyond the core deposit.

200-Metre Trenching Program Delivered Results – The reported samples were collected from trenches excavated over more than 200 metres along the South Zone, where mineralization is described as stibnite associated with brecciated sediments.

Drilling to Follow Up Immediately – The Company said the South Zone will be tested as part of its ongoing spring regional exploration drilling program, with the next phase also including airborne geophysics, soil sampling, mapping, and further trenching.

Broader Bald Hill Expansion Potential – Management said the results support the view that the recently identified “New Zones” could materially expand Bald Hill’s antimony footprint, with a large portion of the 3,700+ hectare property still remaining to be explored.

For more information on Antimony Resources Corp., click here

For more information on the InvestorTalk pre-market series, go to InvestorTalk.com.

{kind=link}