Welcome to the October 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the IEA list of Critical Minerals.

A slowing global economy continues to temper demand for critical minerals in 2023

High interest rates in most Western countries continue to be a drag on the global economy. Last month saw the U.S. Fed pause their interest rate hikes, with the reserve rate still at 5.5%. However, U.S. inflation has been rising again and the Fed has indicated rates will need to stay higher for longer. The September CPI was 3.7%, same as August’s 3.7%, but up on the July 3.2% figure. Long-term bond rates have adjusted higher leading to higher borrowing rates. All of this is slowing the U.S. and much of the global economy therefore not helping EV sales. China’s housing collapse is another negative drag on sentiment and has resulted in slower China EV sales growth in 2023.

Global critical minerals and electric vehicle (“EV”) update

October 2023 saw some better results coming in for global plugin electric car sales which gives some hope that depressed EV metals prices may soon start to recover. Q4 is traditionally the strongest quarter for EV sales with December usually the best sales month of the year.

Global plugin electric car sales were 1,238,000 in August 2023, up 45% on August 2022 sales. Global plugin electric car market share in August was 18%, led by China with 39% share, Europe with 30% share, and USA with 9.51% share. Reports to date suggest that September sales look like being another strong month of about 1.25 million.

2023 sales look set to finish at ~13.5 million and 17% market share, which would be a 28% increase on 2022 (10.522 million and 13% market share). A 28% growth rate in 2023 would be a significant slowdown on the 56% growth rate achieved in 2022.

Global plugin electric car ‘monthly’ sales in 2023

The West is working hard to build up EV and battery capacity rather than being too dependent on China

One of the biggest news of the last month was that Quebec, Canada is in talks with battery makers and automobile companies looking to invest about C$15 billion (US$11 billion) in Quebec over the next three years to support EV supply chains. The report stated:

“Quebec has secured C$15 billion over the past three years and another C$15 billion is coming in the next three years…Over the past three years, Quebec has attracted investments from auto and battery makers such as General Motors, POSCO and Ford Motors. The biggest investment was announced on Thursday when Swedish battery maker Northvolt announced plans to build a $5.2 billion plant in the province.”

While this is good news for the EV and battery manufacturers it does nothing to support the mining industry. It is similar to the U.S. Inflation Reduction Act, where most funds are going to auto and battery companies and very little to the upstream miners. This will only boost demand for critical minerals needed to feed the EV and energy storage booms. Very little is being done to address the looming supply deficits of these critical materials in the second half of the decade.

For example, there are 18 gigafactories planned to be built in the USA this decade, requiring 715,000tpa of lithium, but only 180,000tpa is currently planned. Similar mismatches of supply and demand exist in the pipeline for several other critical metals. Europe’s critical minerals supply chain looks even more dire.

China continues to dominate the EV and battery manufacturing industry

Many people might be unaware that China manufactures ~75-80% of all new global plugin electric cars and ~77% of global lithium-ion batteries. China’s BYD is the world’s largest seller followed by Tesla, who makes over 50% of their cars in China.

In 2022 China had 77% of the lithium-ion battery global capacity

Lithium

China lithium carbonate spot prices fell so far in October 2023, with the price now at CNY 166,500/t (USD 22,781/t) and down 68% over the past year. At these prices, some of the marginal producers in China have begun shutting down. We did get a glimmer of hope for a bottom this week (mid October) as lithium carbonate futures contracts in Guangzhou jumped by 7% to limit up for the day.

Lithium takeovers and equity interests are a leading trend in mid 2023

The biggest news the past month in the lithium sector has been the fight for control of Australia’s Liontown Resources Limited (ASX: LTR), who 100% own the near production Kathleen Valley Lithium Project in Western Australia. U.S. lithium giant Albemarle Corporation (NYSE: ALB) is currently doing due diligence after upping their offer to A$3.00 per share, or about A$6.6 billion (US$4.23 billion) to purchase all of Liontown Resources. However, in recent weeks Australia’s richest woman, Gina Rinehart, via her controlled company Hancock Prospecting, increased its stake in Liontown to 19.9%. Rinehart’s motives are not yet known but it appears the iron ore magnate has become very interested in lithium.

Only 2-3 months back Albemarle bought a 6.4% stake in Canadian lithium junior Patriot Battery Metals Inc. (TSXV: PMET | ASX: PMT | OTCQX: PMETF). The purchase price paid was C$109 million and it was made just one day after Patriot Battery Metals announced their Maiden Resource of 109.2 Mt @ 1.42% Li2O Inferred, the largest lithium spodumene resource in the Americas. The interesting part is that Patriot Battery Metals market cap is only US$866 million, 4.7x lower than Liontown Resources market cap of US$4.068 billion. Liontown Resources resource is about 50% bigger (156Mt at 1.4% Li2O) and about 4 years more advanced than Patriot Battery Metals Corvette Project. Nonetheless, if Albemarle decides to back away from the Liontown Resources takeover bid then there is a very good chance Albemarle will turn their takeover attention towards Patriot Battery Metals.

Mineral Resources Limited (ASX: MIN) has also been very active in 2023 in the lithium space. In September it was confirmed that Mineral Resources is bidding for the liquidated Bald Hill Lithium Mine. Mineral Resources has also backed Develop Global’s takeover offer for Essential Metals Limited (ASX: ESS) for A$152.6 million (US$101 million), plus Mineral Resources has also bought equity stakes in Delta Lithium Ltd. (ASX: DLI) and Global Lithium Resources (ASX: GL1).

Chile’s SQM (NYSE: SQM) also recently made a takeover offer for Azure Minerals Limited (ASX: AZS) for US$585 million.

All of this takeover activity from the major lithium companies suggests that we are near a bottom in the lithium price cycle and that the mid to long term outlook for lithium remains very strong.

Rare Earths

Rare earths supply disruptions have led to some price improvements recently. Neodymium (“Nd”) prices continued their recent recovery so far in mid October 2023 after a rough 2023, currently sitting at CNY 650,000/t.

Rare earths prices have been falling for most of 2023; however recent supply disruptions in Myanmar have caused most rare earth prices to strengthen. There have also been some reports that Malaysia is developing a policy to ban exports of rare earths raw materials so as to boost their domestic industry. There is no date given yet as to when a ban may start. In any event, Myanmar is a much more important supplier than Malaysia.

This month Australian Strategic Materials Limited (ASX: ASM) announced some world-class test work results with their terbium (Tb) and dysprosium (Dy) heavy rare earth separation test work. Pilot plant test work produced “>99.99% for Tb and > 99.95% for Dy1, at steady state”. Results like this from their Dubbo Project ore should give some more impetus to getting the Dubbo Project financed with probable output of around 140tpa Dy and 20tpa Tb. ASM Managing Director, Miss Rowena Smith stated:

“These excellent results demonstrate the strength of ASM’s advanced technical capability…Terbium and dysprosium oxides are not only scarce commodities they are very difficult to separate at high purity. With the continued expertise of the team at ANSTO and the welcome support of the NSW Government, we are positioning the Dubbo Project to be at the forefront of Australia’s rare earth and critical minerals evolution.”

Dysprosium is a key rare earth used in nuclear reactor control rods and neodymium-iron-boron permanent magnets used in many EVs and wind turbines. Terbium is used in fluorescent lamps and television and monitor cathode-ray tubes.

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$14.84/lb) remained flat the past month and continue to be very depressed. China’s demand for NMC cathode material for EVs has been weak, not helped by the popularity of LFP cathodes that don’t use nickel or cobalt.

Flake graphite prices remain very weak with prices near the marginal cost of production. A combination of slower EV sales growth in 2023 and increased China graphite supply has led to a depressed graphite market. Macquarie and others forecast graphite to start heading into deficit from about 2024.

Nickel prices have recently weakened further due to oversupply concerns from Indonesia and a slowing Chinese property sector.

Manganese prices remain weak mostly due to weak Chinese demand as the Chinese housing industry continues to rebalance after years of over construction and oversupply.

Longer term the outlook for the EV and energy stationary storage (“ESS”) sectors looks extremely strong. This is expected to lead to a huge surge in demand for the critical metals that supply these sectors.

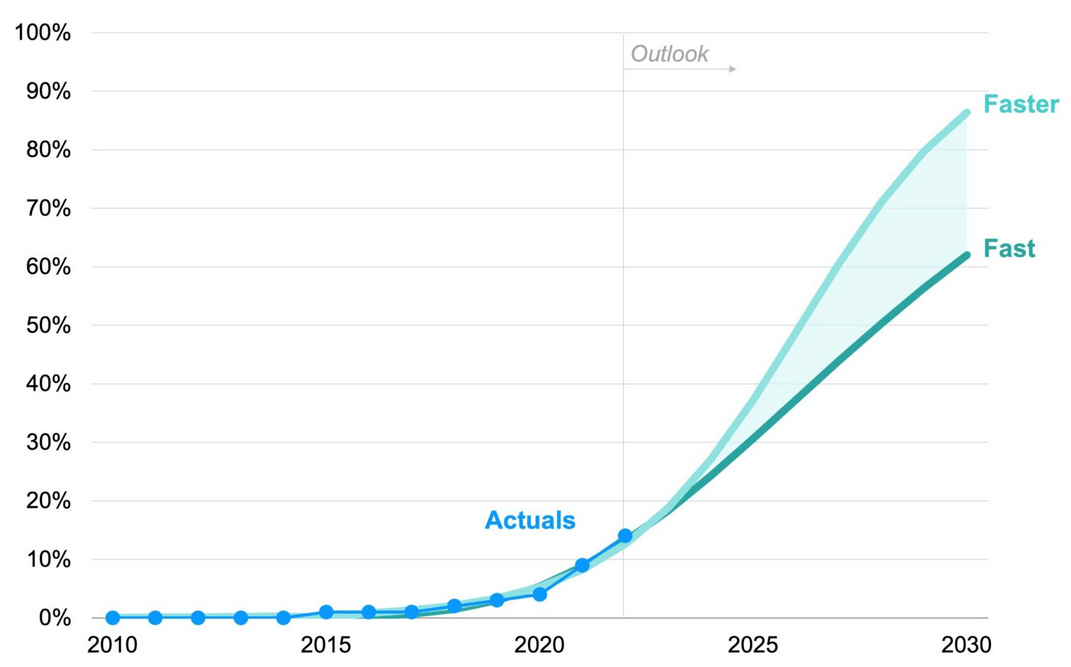

EV sales are forecast to increase to somewhere between 62% and 86% market share of global car sales by 2030

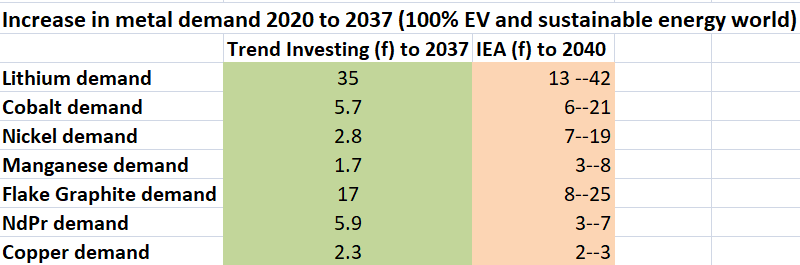

Trend Investing v IEA demand forecast for EV metals

Source: Trend Investing and the IEA

Latest CMI events

- Friday October 20, 2023 – CMI Masterclass: Critical Minerals in the Congo. Details and event tickets here.

{kind=link}

{kind=link}

Leave a Reply